Last Update 19 hours ago Total Questions : 287

The Exam I: Finance Theory Financial Instruments Financial Markets - 2015 Edition content is now fully updated, with all current exam questions added 19 hours ago. Deciding to include 8006 practice exam questions in your study plan goes far beyond basic test preparation.

You'll find that our 8006 exam questions frequently feature detailed scenarios and practical problem-solving exercises that directly mirror industry challenges. Engaging with these 8006 sample sets allows you to effectively manage your time and pace yourself, giving you the ability to finish any Exam I: Finance Theory Financial Instruments Financial Markets - 2015 Edition practice test comfortably within the allotted time.

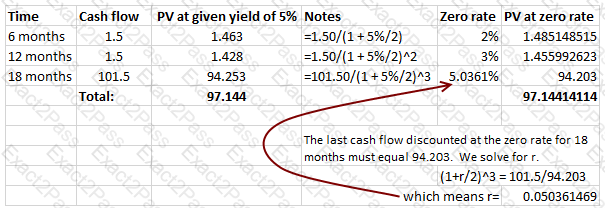

The yield offered by a bond with 18 months remaining to maturity is 5%. The coupon is 3%, paid semi-annually, and there are two more coupon payments to go in addition to the interest payment made at maturity. The zero rate for 6 months is 2%, that for 12 months is 3%. What is the 18 month zero rate?

Which of the following have a negative gamma:

I. a long call position

II. a short put position

III. a short call position

IV. a long put position

The gamma in a commodity futures contract is:

An investor can use which of the following to replicate a fixed for floating interest rate swap where the investor pays fixed and receives floating?

I. Long positions in a series of forward rate agreements (FRAs)

II. A short position in a fixed rate bond and a long position in a floating rate note

III. A long position in a floating rate note and a short position in an FRA

IV. A long position in an interest rate cap and a short position in an interest rate floor at the same strike

Security A and B both have expected returns of 10%, but the standard deviation of Security A is 10% while that of security B is 20%. Borrowings are not permitted. A portfolio manager who wishes to maximize his probability of earning a 25% return during the year should invest in:

Which of the following statements are true for a portfolio of two assets:

I. Given volatility, weights and correlation, combined standard deviation cannot be calculated without additional information on covariances.

II. When the two assets are perfectly negatively correlated, the standard deviation of the combined portfolio is just the weighted average of their standard deviations, weighted by their weights in the portfolio.

III. When the two assets are uncorrelated, the standard deviation of the combined portfolio is just the weighted average of their standard deviations, weighted by their weights in the portfolio.

IV. When the two assets are perfectly positively correlated, the standard deviation of the combined portfolio is just the weighted average of their standard deviations, weighted by their weights in the portfolio.

Backwardation in commodity futures is explained by:

Backwardation can be explained by:

A bank advertises its certificates of deposits as yielding a 5.2% annual effective rate. What is the equivalent continuously compounded rate of return?

[According to the PRMIA study guide for Exam 1, Simple Exotics and Convertible Bonds have been excluded from the syllabus. You may choose to ignore this question. It appears here solely because the Handbook continues to have these chapters.]

Which of the following statements relating to convertible debt are true:

I. A hard call protection means the bond cannot be called by the issuer till the share price reaches a threshold

II. It is advantageous for the issuer to call its convertible securities when the share price exceeds the conversion price

III. When the issuer ' s share prices is very high, the convertible bond trades at a discount to the value of the shares it is convertible into

IV. Convertible bonds generally have to carry a higher coupon than on equivalent non-convertible securities to make them attractive to investors