Last Update 23 hours ago Total Questions : 240

The Operational Risk Manager (ORM) Exam content is now fully updated, with all current exam questions added 23 hours ago. Deciding to include 8010 practice exam questions in your study plan goes far beyond basic test preparation.

You'll find that our 8010 exam questions frequently feature detailed scenarios and practical problem-solving exercises that directly mirror industry challenges. Engaging with these 8010 sample sets allows you to effectively manage your time and pace yourself, giving you the ability to finish any Operational Risk Manager (ORM) Exam practice test comfortably within the allotted time.

A key problem with return on equity as a measure of comparative performance is:

Which of the following statements are true:

I. A transition matrix is the probability of a security migrating from one rating class to another during its lifetime.

II. Marginal default probabilities refer to probabilities of default in a particular period, given survival at the beginning of that period.

III. Marginal default probabilities will always be greater than the corresponding cumulative default probability.

IV. Loss given default is generally greater when recovery rates are low.

Which of the following best describes Altman's Z-score

There are three bonds in a diversified bond portfolio, whose default probabilities are independent of each other and equal to 1%, 2% and 3% respectively over a 1 year time horizon. Calculate the probability that exactly 1 of the three bonds will default.

Which of the following belong in a credit risk report?

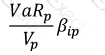

Which of the following formulae describes Marginal VaR for a portfolio p, where V_i is the value of the i-th asset in the portfolio? (All other notation and symbols have their usual meaning.)

A)

B)

C)

D)

All of the above

Which of the following is true in relation to the application of Extreme Value Theory when applied to operational risk measurement?

I. EVT focuses on extreme losses that are generally not covered by standard distribution assumptions

II. EVT considers the distribution of losses in the tails

III. The Peaks-over-thresholds (POT) and the generalized Pareto distributions are used to model extreme value distributions

IV. EVT is concerned with average losses beyond a given level of confidence

Which of the following statements are correct in relation to the financial system just prior to the current financial crisis:

I. The system was robust against small random shocks, but not against large scale disturbances to key hubs in the network

II. Financial innovation helped reduce the complexity of the financial network

III. Knightian uncertainty refers to risk that can be quantified and measured

IV. Feedback effects under stress accentuated liquidity problems

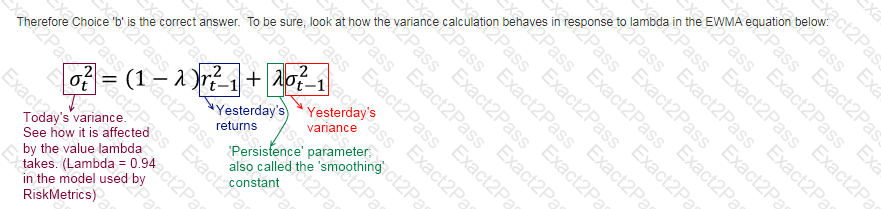

As the persistence parameter under EWMA is lowered, which of the following would be true:

If F be the face value of a firm's debt, V the value of its assets and E the market value of equity, then according to the option pricing approach a default on debt occurs when: