Last Update 19 hours ago Total Questions : 287

The PRM Exam 1: Finance Foundations content is now fully updated, with all current exam questions added 19 hours ago. Deciding to include 8013 practice exam questions in your study plan goes far beyond basic test preparation.

You'll find that our 8013 exam questions frequently feature detailed scenarios and practical problem-solving exercises that directly mirror industry challenges. Engaging with these 8013 sample sets allows you to effectively manage your time and pace yourself, giving you the ability to finish any PRM Exam 1: Finance Foundations practice test comfortably within the allotted time.

Basis risk between spot and futures prices for stock indices is caused by changes in:

I. The risk free rate, or the funding cost for the futures

II. Expected dividend yield

III. Volatility of the underlying stock index

Which of the following statements are true:

I. The Kappa family of indices take only downside risk into account

II. The Treynor ratio provides information on the excess return per unit of specific risk

III. All else remaining constant, the Sharpe ratio for a portfolio will increase as we increase leverage by borrowing and investing in the risky bundle

IV. In the market portfolio, we can expect Jensen's alpha to equal zero.

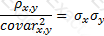

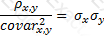

The relationship between covariance and correlation for two assets x and y is expressed by which of the following equations (where covar x,y is the covariance between x and y , σ x and σ y are the respective standard deviations and ρ x,y is the correlation between x and y ):

A)

B)

C)

D)

None of the above

Which of the following does not explain the shape of an yield curve?

What would be the expected return on a stock with a beta of 1.2, when the risk free rate is 3% and the broad market index is expected to earn 8%?

Which of the following statements are true:

I. An yield curve plots zero coupon spot rates for different maturities for bonds with different credit ratings

II. An yield curve represents the term structure of interest rates for similar instruments across a range of maturities

III. The liquidity preference theory explains why the yield curve can be downward sloping

IV. The term structure refers to the relationship between bond yields and bond maturities

Which of the following statements are true:

I. Caps allow the buyer of the cap protection against rise in interest expense

II. Floors offer investors protection from downward movement in interest rates

III. Collars can be used as hedges

IV. Both caps and collars can be used to hedge against widening credit spreads

For a pair of correlated assets, the achievable portfolio standard deviation will be the lowest when the correlation ρ is:

If the quoted discount rate of a 3 month treasury bill futures contract is 10%, what is the price of a 3-month treasury bill with a principal at maturity of $100?

[According to the PRMIA study guide for Exam 1, Simple Exotics and Convertible Bonds have been excluded from the syllabus. You may choose to ignore this question. It appears here solely because the Handbook continues to have these chapters.]

A digital cash-or-nothing option can be hedged reasonably effectively using: