Last Update 19 hours ago Total Questions : 287

The PRM Exam 1: Finance Foundations content is now fully updated, with all current exam questions added 19 hours ago. Deciding to include 8013 practice exam questions in your study plan goes far beyond basic test preparation.

You'll find that our 8013 exam questions frequently feature detailed scenarios and practical problem-solving exercises that directly mirror industry challenges. Engaging with these 8013 sample sets allows you to effectively manage your time and pace yourself, giving you the ability to finish any PRM Exam 1: Finance Foundations practice test comfortably within the allotted time.

Assuming all other factors remain the same, an increase in the volatility of the returns on the assets of a firm causes which of the following outcomes?

A 'consol' is a perpetual bond issued by the UK government. Its running yield is 5%. What is its duration?

An investor enters into a 4 year interest rate swap with a bank, agreeing to pay a fixed rate of 4% on a notional of $100m in return for receiving LIBOR. What is the value of the swap to the investor two years hence, immediately after the net interest payments are exchanged? Assume the 2 year swap rate is 5%, and the yield curve is also flat at 5%

The yield offered by a bond with 18 months remaining to maturity is 5%. The coupon is 3%, paid semi-annually, and there are two more coupon payments to go in addition to the interest payment made at maturity. What is the bond's price?

A trader comes in to work and finds the following prices in relation to a stock: $100 spot, $10 for a call expiring in one year with a strike price of $100, and $10 for a put with the same expiry and strike. Interest rates are at 5% per year, and the stock does not pay any dividends. What should the trader do?

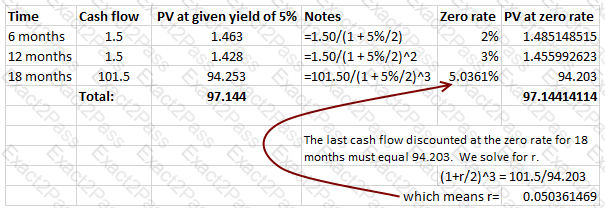

The yield offered by a bond with 18 months remaining to maturity is 5%. The coupon is 3%, paid semi-annually, and there are two more coupon payments to go in addition to the interest payment made at maturity. The zero rate for 6 months is 2%, that for 12 months is 3%. What is the 18 month zero rate?

Which of the following is not a money market security

Which of the following statements are true:

The greatest risk in energy derivatives trading comes from:

A bank advertises its certificates of deposits as yielding a 5.2% annual effective rate. What is the equivalent continuously compounded rate of return?