Last Update 6 hours ago Total Questions : 362

The PRM Certification - Exam III: Risk Management Frameworks, Operational Risk, Credit Risk, Counterparty Risk, Market Risk, ALM, FTP - 2015 Edition content is now fully updated, with all current exam questions added 6 hours ago. Deciding to include 8008 practice exam questions in your study plan goes far beyond basic test preparation.

You'll find that our 8008 exam questions frequently feature detailed scenarios and practical problem-solving exercises that directly mirror industry challenges. Engaging with these 8008 sample sets allows you to effectively manage your time and pace yourself, giving you the ability to finish any PRM Certification - Exam III: Risk Management Frameworks, Operational Risk, Credit Risk, Counterparty Risk, Market Risk, ALM, FTP - 2015 Edition practice test comfortably within the allotted time.

If the duration of a bond yielding 10% is 6 years, the volatility of the underlying interest rates 5% per annum, what is the 10-day VaR at 99% confidence of a bond position comprising just this bond with a value of $10m? Assume there are 250 days in a year.

For a given notional amount, which of the following carries the greatest counterparty exposure (assuming the same counterparty credit rating for each):

Which of the following are likely to be useful to a risk manager analyzing liquidity risk for an international bank?

I. Information on liquidity mismatches

II. Funding concentration

III. Lending concentration

IV. A report on illiquid assets

Which of the following statements are true in relation to Historical Simulation VaR?

I. Historical Simulation VaR assumes returns are normally distributed but have fat tails

II. It uses full revaluation, as opposed to delta or delta-gamma approximations

III. A correlation matrix is constructed using historical scenarios

IV. It particularly suits new products that may not have a long time series of historical data available

When performing portfolio stress tests using hypothetical scenarios, which of the following is not generally a challenge for the risk manager?

There are three bonds in a diversified bond portfolio, whose default probabilities are independent of each other and equal to 1%, 2% and 3% respectively over a 1 year time horizon. Calculate the probability that none of the three bonds will default.

Which of the following statements is the most appropriate description of feedback effects:

If an institution has $1000 in assets, and $800 in liabilities, what is the economic capital required to avoid insolvency at a 99% level of confidence? The VaR in respect of the assets at 99% confidence over a one year period is $100.

Which of the following will be a loss not covered by operational risk as defined under Basel II?

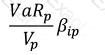

Which of the following formulae describes Marginal VaR for a portfolio p, where V_i is the value of the i-th asset in the portfolio? (All other notation and symbols have their usual meaning.)

A)

B)

C)

D)

All of the above