Last Update 1 hour ago Total Questions : 240

The Operational Risk Manager (ORM) Exam content is now fully updated, with all current exam questions added 1 hour ago. Deciding to include 8010 practice exam questions in your study plan goes far beyond basic test preparation.

You'll find that our 8010 exam questions frequently feature detailed scenarios and practical problem-solving exercises that directly mirror industry challenges. Engaging with these 8010 sample sets allows you to effectively manage your time and pace yourself, giving you the ability to finish any Operational Risk Manager (ORM) Exam practice test comfortably within the allotted time.

Which of the following is not a limitation of the univariate Gaussian model to capture the codependence structure between risk factros used for VaR calculations?

Which of the following best describes economic capital?

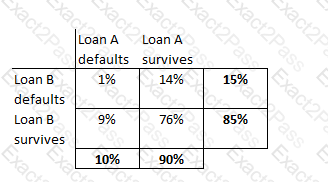

A portfolio has two loans, A and B, each worth $1m. The probability of default of loan A is 10% and that of loan B is 15%. The probability of both loans defaulting together is 1%. Calculate the expected loss on the portfolio.

Economic capital under the Earnings Volatility approach is calculated as:

Which of the below are a way to classify risk governance structures:

A Reactive, Preventative and Active

B. Committee based, regulation based and board mandated

C. Top-down and Bottom-up

D. Active and Passive

The Basel framework does not permit which of the following Units of Measure (UoM) for operational risk modeling:

I. UoM based on legal entity

II. UoM based on event type

III. UoM based on geography

IV. UoM based on line of business

Loss from a lawsuit from an employee due to physical harm caused while at work is categorized per Basel II as:

Which of the following is not a risk faced by a bank from holding a portfolio of residential mortgages?

The unexpected loss for a credit portfolio at a given VaR estimate is defined as:

Which of the following statements are true:

I. The set of UoMs used for frequency and severity modeling should be identical

II. UoMs can be grouped together into larger combined UoMs using judgment based on the knowledge of the business

III. UoMs can be grouped together into combined UoMs using statistical techniques

IV. One may use separate sets of UoMs for frequency and severity modeling