Last Update 1 hour ago Total Questions : 240

The Operational Risk Manager (ORM) Exam content is now fully updated, with all current exam questions added 1 hour ago. Deciding to include 8010 practice exam questions in your study plan goes far beyond basic test preparation.

You'll find that our 8010 exam questions frequently feature detailed scenarios and practical problem-solving exercises that directly mirror industry challenges. Engaging with these 8010 sample sets allows you to effectively manage your time and pace yourself, giving you the ability to finish any Operational Risk Manager (ORM) Exam practice test comfortably within the allotted time.

Which of the following are ordered correctly in the order of debt seniority in a bankruptcy situation?

I. Equity, Subordinate debt, Senior debt

II. Senior debt, Preferred stock, Equity

III. Secured debt, Accounts payable, Preferred stock

IV. Secured debt, DIP financing, Equity

Which of the following statements is true:

I. When averaging quantiles of two Pareto distributions, the quantiles of the averaged models are equal to the geometric average of the quantiles of the original models based upon the number of data items in each original model.

II. When modeling severity distributions, we can only use distributions which have fewer parameters than the number of datapoints we are modeling from.

III. If an internal loss data based model covers the same risks as a scenario based model, they can can be combined using the weighted average of their parameters.

IV If an internal loss model and a scenario based model address different risks, the models can be combined by taking their sums.

Which loss event type is the failure to timely deliver collateral classified as under the Basel II framework?

If E denotes the expected value of a loan portfolio at the end on one year and U the value of the portfolio in the worst case scenario at the 99% confidence level, which of the following expressions correctly describes economic capital required in respect of credit risk?

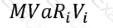

Which of the formulae below describes incremental VaR where a new position 'm' is added to the portfolio? (where p is the portfolio, and V_i is the value of the i-th asset in the portfolio. All other notation and symbols have their usual meaning.)

A)

B)

C)

D)

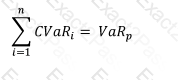

If the full notional value of a debt portfolio is $100m, its expected value in a year is $85m, and the worst value of the portfolio in one year's time at 99% confidence level is $60m, then what is the credit VaR?

According to the Basel framework, reserves resulting from the upward revaluation of assets are considered a part of:

For a back office function processing 15,000 transactions a day with an error rate of 10 basis points, what is the annual expected loss frequency (assume 250 days in a year)

A derivative contract has a negative current replacement value. Which of the following statements is true about its loan equivalent value for credit risk calculations over a 2-year horizon?

Which of the following are valid approaches to calculating potential future exposure (PFE) for counterparty risk:

I. Add a percentage of the notional to the mark-to-market value

II. Monte Carlo simulation

III. Maximum Likelihood Estimation

IV. Parametric Estimation