Last Update 20 hours ago Total Questions : 328

The Credit and Counterparty Manager (CCRM) Certificate Exam content is now fully updated, with all current exam questions added 20 hours ago. Deciding to include 8011 practice exam questions in your study plan goes far beyond basic test preparation.

You'll find that our 8011 exam questions frequently feature detailed scenarios and practical problem-solving exercises that directly mirror industry challenges. Engaging with these 8011 sample sets allows you to effectively manage your time and pace yourself, giving you the ability to finish any Credit and Counterparty Manager (CCRM) Certificate Exam practice test comfortably within the allotted time.

Which of the following are measures of liquidity risk

I. Liquidity Coverage Ratio

II. Net Stable Funding Ratio

III. Book Value to Share Price

IV. Earnings Per Share

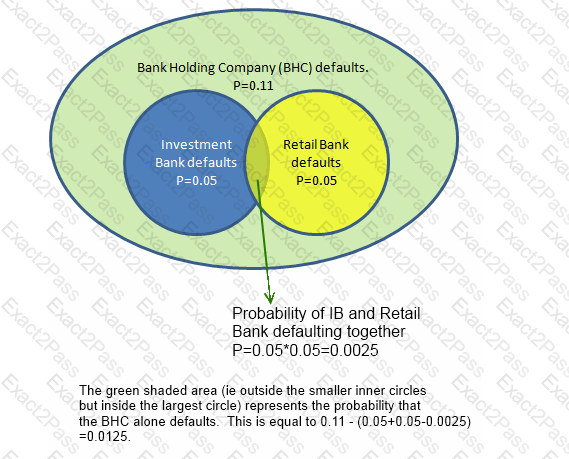

A Bank Holding Company (BHC) is invested in an investment bank and a retail bank. The BHC defaults for certain if either the investment bank or the retail bank defaults. However, the BHC can also default on its own without either the investment bank or the retail bank defaulting. The investment bank and the retail bank's defaults are independent of each other, with a probability of default of 0.05 each. The BHC's probability of default is 0.11.

What is the probability of default of both the BHC and the investment bank? What is the probability of the BHC's default provided both the investment bank and the retail bank survive?

Which of the following distribution assumptions will produce the lowest probability of exceeding an extreme value, assuming identical means and variances?

Which of the following represent the parameters that define a VaR estimate?

Which of the following is not a risk faced by a bank from holding a portfolio of residential mortgages?

A derivative contract has a negative current replacement value. Which of the following statements is true about its loan equivalent value for credit risk calculations over a 2-year horizon?

Which of the following steps are required for computing the aggregate distribution for a UoM for operational risk once loss frequency and severity curves have been estimated:

I. Simulate number of losses based on the frequency distribution

II. Simulate the dollar value of the losses from the severity distribution

III. Simulate random number from the copula used to model dependence between the UoMs

IV. Compute dependent losses from aggregate distribution curves

If the cumulative default probabilities of default for years 1 and 2 for a portfolio of credit risky assets is 5% and 15% respectively, what is the marginal probability of default in year 2 alone?

In respect of operational risk capital calculations, the Basel II accord recommends a confidence level and time horizon of:

Which of the following are valid techniques used when performing stress testing based on hypothetical test scenarios:

I. Modifying the covariance matrix by changing asset correlations

II. Specifying hypothetical shocks

III. Sensitivity analysis based on changes in selected risk factors

IV. Evaluating systemic liquidity risks

A diagram of a bank

Description automatically generated

A diagram of a bank

Description automatically generated