Last Update 20 hours ago Total Questions : 328

The Credit and Counterparty Manager (CCRM) Certificate Exam content is now fully updated, with all current exam questions added 20 hours ago. Deciding to include 8011 practice exam questions in your study plan goes far beyond basic test preparation.

You'll find that our 8011 exam questions frequently feature detailed scenarios and practical problem-solving exercises that directly mirror industry challenges. Engaging with these 8011 sample sets allows you to effectively manage your time and pace yourself, giving you the ability to finish any Credit and Counterparty Manager (CCRM) Certificate Exam practice test comfortably within the allotted time.

Random recovery rates in respect of credit risk can be modeled using:

Which of the following statements is true?

I. Real Time Gross Systems (RTGS) for large value payments consume less system liquidity than Deferred Net Systems (DNS)

II. The US Fedwire is an example of a Real Time Gross System

III. Current disclosure requirements in relation to liquidity risk as laid down in the Basel framework require banks to disclose how liquidity stress scenarios were formulated

IV. A CFP (Contingency Funding Plan) provides access to Central Bank financing

If the loss given default is denoted by L, and the recovery rate by R, then which of the following represents the relationship between loss given default and the recovery rate?

Which of the following statements are true in relation to Historical Simulation VaR?

I. Historical Simulation VaR assumes returns are normally distributed but have fat tails

II. It uses full revaluation, as opposed to delta or delta-gamma approximations

III. A correlation matrix is constructed using historical scenarios

IV. It particularly suits new products that may not have a long time series of historical data available

Which of the following introduces model error when basing VaR on a normal distribution with a static mean and standard deviation?

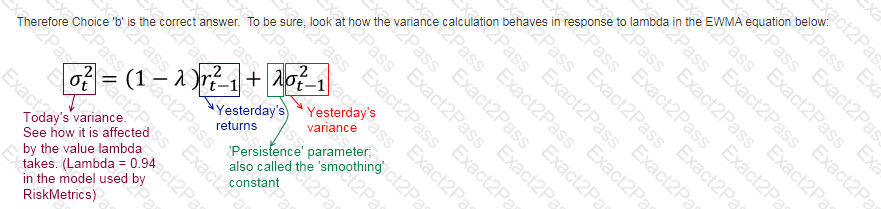

As the persistence parameter under EWMA is lowered, which of the following would be true:

Credit exposure for derivatives is measured using

Which of the following statements are true in relation to the current state of the financial network?

I. Interconnectivity between countries has reduced while that between institutions in the same country has increased significantly

II. The degrees of separation between institutions has gone up

III. The average path length connecting any two given institutions has shrunk

IV. Knife-edge dynamics imply that systemic risk arises from the financial system flipping from risk sharing to risk spreading

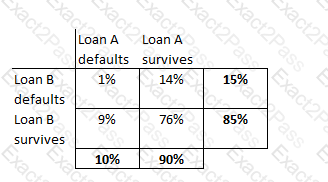

A portfolio has two loans, A and B, each worth $1m. The probability of default of loan A is 10% and that of loan B is 15%. The probability of both loans defaulting together is 1%. Calculate the expected loss on the portfolio.

Which of the following are considered counterparty based credit enhancements?

I. Collateral

II. Credit default swaps

III. Close out netting arrangements

IV. Guarantees

A white background with red and green text

Description automatically generated

A white background with red and green text

Description automatically generated A white rectangular grid with black text

Description automatically generated

A white rectangular grid with black text

Description automatically generated