Last Update 20 hours ago Total Questions : 328

The Credit and Counterparty Manager (CCRM) Certificate Exam content is now fully updated, with all current exam questions added 20 hours ago. Deciding to include 8011 practice exam questions in your study plan goes far beyond basic test preparation.

You'll find that our 8011 exam questions frequently feature detailed scenarios and practical problem-solving exercises that directly mirror industry challenges. Engaging with these 8011 sample sets allows you to effectively manage your time and pace yourself, giving you the ability to finish any Credit and Counterparty Manager (CCRM) Certificate Exam practice test comfortably within the allotted time.

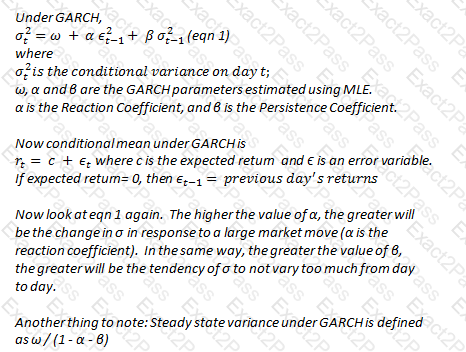

A risk analyst uses the GARCH model to forecast volatility, and the parameters he uses are ω = 0.001%, α = 0.05 and β = 0.93. Yesterday's daily volatility was calculated to be 1%. What is the long term annual volatility under the analyst's model?

Under the standardized approach to determining operational risk capital, operations risk capital is equal to:

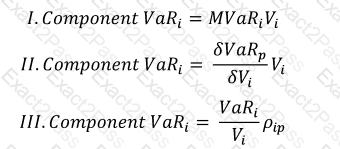

Which of the following formulae correctly describes Component VaR. (p refers to the portfolio, and i is the i-th constituent of the portfolio. MVaR means Marginal VaR, and other symbols have their usual meanings.)

A risk analyst analyzing the positions for a proprietary trading desk determines that the combined annual variance of the desk's positions is 0.16. The value of the portfolio is $240m. What is the 10-day stand alone VaR in dollars for the desk at a confidence level of 95%? Assume 250 trading days in a year.

Which of the following cannot be used to address the issue of heavy tails when modeling market returns

A risk analyst peforming PCA wishes to explain 80% of the variance. The first orthogonal factor has a volatility of 100, and the second 40, and the third 30. Assume there are no other factors. Which of the factors will be included in the final analysis?

When estimating the risk of a portfolio of equities using the portfolio's beta, which of the following is NOT true:

The VaR of a portfolio at the 99% confidence level is $250,000 when mean return is assumed to be zero. If the assumption of zero returns is changed to an assumption of returns of $10,000, what is the revised VaR?

If the default hazard rate for a company is 10%, and the spread on its bonds over the risk free rate is 800 bps, what is the expected recovery rate?

Once the frequency and severity distributions for loss events have been determined, which of the following is an accurate description of the process to determine a full loss distribution for operational risk?

A white text with black text

Description automatically generated

A white text with black text

Description automatically generated