Last Update 13 hours ago Total Questions : 45

The Strategic Case Study Exam 2021 content is now fully updated, with all current exam questions added 13 hours ago. Deciding to include CS3 practice exam questions in your study plan goes far beyond basic test preparation.

You'll find that our CS3 exam questions frequently feature detailed scenarios and practical problem-solving exercises that directly mirror industry challenges. Engaging with these CS3 sample sets allows you to effectively manage your time and pace yourself, giving you the ability to finish any Strategic Case Study Exam 2021 practice test comfortably within the allotted time.

You have just received the following email:

From: William Seaton, Director of Finance

To: Finance Manager

Subject: Oil reserves

Hi,

This email arrived from the Head Geologist earlier today. I am concerned that many of our colleagues understand very little other than rock formations and drilling reports. They certainly misunderstand accounting issues. I have already had some very confused discussions with the other members of the Board.

I need a very clear report from you that I can circulate to the other Board members. I am not particularly interested in the technical accounting rules. I do not think that you necessarily require an accounting standard to tell you that a particular disclosure is misleading.

I need your report to cover the following:

Should we make a public announcement of this information? I would like a clear indication of the implications for our

relationship with our various stakeholders AND the ethical issues that you feel are relevant.

What are the implications for our share price? I would like your analysis to consider the factors that will indicate how

our share price will change upon the announcement.

Thanks

William

The email referred to above can be found by clicking on the Reference Materials button.

Press clipping from today’s Financial News:

Yesterday’s announcement of yet another major oil find by Slide should keep everybody happy. Nobody will be happier than the directors of Fouce Oil, whose continuing ownership of one quarter of Slide’s shares continues to confuse industry insiders. Perhaps there are hidden depths to the relationship between Slide and Fouce Oil.

Three months has passed since the discussion concerning Fouce Oil’s proposal.

You have received the following email from William Seaton, Director of Finance:

From: William Seaton, Director of Finance

To: Finance Manager

Subject: Fouce Oil’s proposal to collaborate on exploration

Hi,

After deliberating at length on the various discussions that we have had with Fouce Oil since its initial approach, we have decided to proceed.

We need to work out some important details, otherwise this venture will be a disaster.

Please draft a report that covers the following matters:

Should we create a formal coaching and mentoring scheme, whereby members of Fouce Oil’s exploration staff will receive guidance from their counterparts at Slide? Please explain the advantages and disadvantages of doing so very clearly.

Please explain how best to organise a formal coaching and mentoring scheme, if we decide that we should create one.

How should we manage the business relationship between the two companies’ exploration staff for the duration of this arrangement?

What are the difficulties associated with decision-making on exploration issues and how should we address those?

The collaboration goes live in a few weeks and so I need your input urgently so that I can get things moving.

William

It is now three days since the start of the oil spillage crisis.

You have received the following email from William Seaton, Director of Finance:

From: William Seaton, Director of Finance

To: Finance Manager

Subject: Crisis management issues

Hi,

A quick update on the latest developments.

We have brought Block Associates in to lead the operations on dealing with the oil spill. It has assigned one of its leading consultants to take charge of this for us. We have paid Block Associates an annual retainer for many years, but we have never actually had to call on its services because we have been able to contain any environmental problems using our own resources.

Using Block Associates is going to be expensive. It insists on being free to bring in whatever equipment and personnel are required to resolve matters and to charge that on the basis of cost plus 25%. Our annual retainer is simply the cost of ensuring that it will respond on this basis if required.

We have had some murmurings of discontent already because our own engineers and geologists have made significant progress in identifying the cause of the spillage and they believe that they are capable of bringing it to a successful conclusion. They have suggested that it would be both quicker and cheaper to leave them in charge, while retaining the option to bring in Block Associates at a later date if they fail.

Firstly, what factors should we take into account in deciding whether to leave our own experts in charge of this operation rather than using Block Associates?

Secondly, how should we manage our relationship with Block Associates if we decide that it should be used?

Thirdly, two things: The Board is concerned that Slide’s engineers and geologists have already become disillusioned by the decision to consider calling in Block Associates. We cannot afford to lose their commitment or to see them decide to leave Slide in the longer term. I need you to provide me with some ideas as to how we can motivate them to give their best performance for the duration of this crisis AND to inspire them to remain in Slide’s employment after the crisis has been resolved.

William

Newsweb

Protesters block bulldozers

Attempts by Wodd to harvest some of the hardwood trees from their newly acquired Bravadorian forest suffered a further setback yesterday.

Wodd’s bulldozers have been unable to make any headway in clearing the site for the company’s first logging base because environmental groups from several countries have descended on the Bravadorian jungle to protest the proposed destruction of the forest and the associated harvesting of many rare hardwood trees. Protestors have chained themselves to trees and to heavy equipment, making it impossible to commence the clearance operations.

Wodd’s problems have been compounded by the recent discovery that a tribe of forest dwellers has lived in the forest for many generations, making little or no contact with the outside world in the process. The tribe is effectively nomadic, moving from one part of the forest to another, surviving by hunting game and gathering edible vegetation and relocating when food starts to become scarce. The environmental protestors claim that Wodd’s activities will make it impossible for this tribe to continue with its traditional way of life.

Wodd claims to adhere to The Forestry Stewardship Council of Marland’s ten principles, which include the assurance that " The legal and customary rights of indigenous peoples to own, use and manage their lands, territories, and resources shall be recognized and respected. "

Reference Material:

A month later, you receive the following email:

Reference Material:

From: Hesham El-Sayed. Independent Non-executive

Director

To: Romuald Marek. Chief Finance Officer

Subject: Collapse of fuel supplier

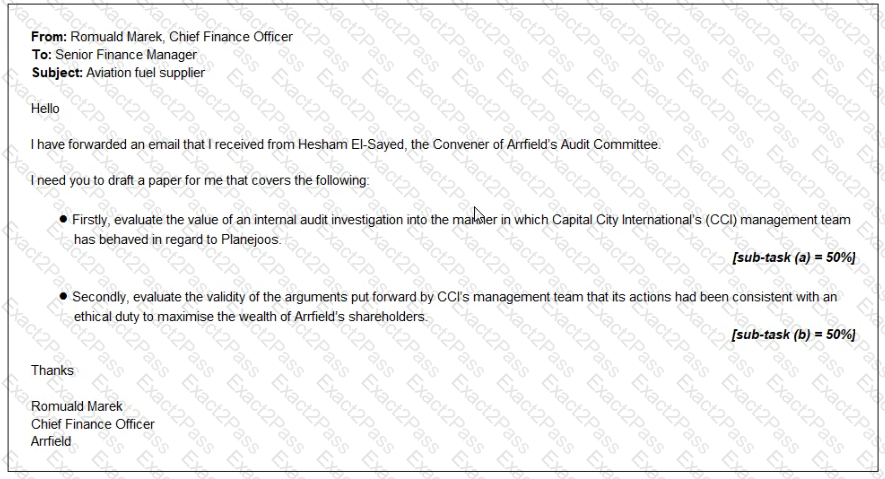

Hi Romuald

I am writing to give you some advance notice of an internal audit investigation that has been commissioned by the Audit Committee

Just over a year ago. Planej oos, a newly formed company, approached the management team at Airfield ' s Capital City International (CCI) airport and offered to take over refueling operations at Starport Planejoos offered a higher percentage of revenue than the existing supplier was pay ing CCI ' s management team agreed and appointed Planejoos rather than renew the existing supplier ' s contract.

CCI was unable to conduct the usual background and credit checks on Planejoos for two reasons. Firstly, Planejoos was a new company and so did not have an extensive credit history that could be checked Secondly CCI was under time pressure to reach a decision on whether to renew the existing supplier ' s contract or allow it to expire

CCI ' s management team claimed that it had acted quickly in order to benefit from the additional revenue that could be earned from dealing with Planejoos The management team was acting on the basis that it had an ethical duty to maximise the wealth of Airfield ' s shareholders and that maximising revenues from fuel sales t hrough this agreement with Planejoos was consistent with that ethical duty.

Unfortunately, as a new company. Planejoos struggled to obtain trade credit and the high demand for fuel put the company ' s cash flows under extreme pressure Receipts from sales la gged behind payments for inventory Planejoos has now collapsed, leaving a large trade receivable that CCI will have to write off as uncollectable CCI had permitted this receivable to accumulate rather

than pressing for payment and so putting Planejoos und er further pressure.

Fortunately, the previous fuel supplier was prepared to return to CCI.

Kind regards

Hello

I have attached a news article

Arrfield does not set the price for aviation fuel sold at our airports, but we do receive a percentage of the revenues earned by the fuel companies.

I need your help to prepare for a Board meeting to discuss this matter Please write a paper covering the following

* Firstly, explain the impact that the criticisms voiced by the environmental campaigners will have on the frequent PESTEL analysis that Arrfield ' s Board conducts.

[sub-task (a) = 34%

* Secondly, evaluate the commercial logic of Arrfield ' s strategy of basing charges for non-aeronautical services (such as fuel sales and retail activities) on percentages of the revenues generated by the companies that operate at its airports

[sub-task (b) = 33%)

* Thirdly, recommend with reasons whether Arrfield should attempt to justify strategic decisions to its shareholders when the commercial logic of those decisions is not immediately obvious

[sub-task (c) = 33%}

Thanks

Romuald Marek

Chief Finance Offi cer

A week later, Romuald Marek stops by your workspace and hands you a document.

The Board minute extract from Romuald can be viewed by clicking the Reference Material button above.

Reference Material

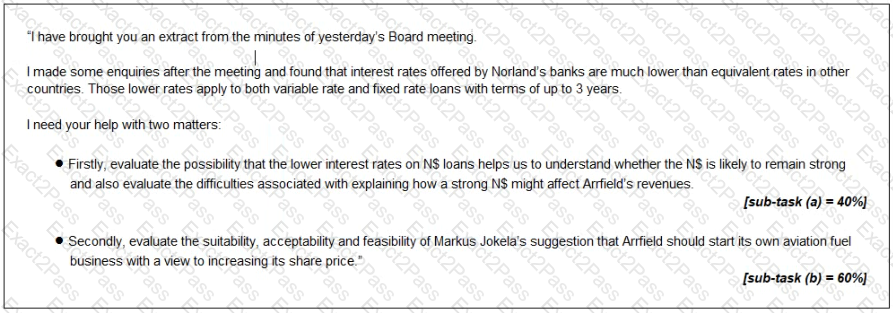

Board minutes extract: proposal to profit from ongoing strength of NS

Anna Obalowu Sole, Chief Operating Officer, reported that the strong NS was helping generate revenues from fuel sales. Discussion followed as to whether the strong N$ was likely to persist and whether a strong N$ benefits Arrfield overall.

Markus Jokela. Chief Executive Officer, stated that the Board should develop contingency plans that could be implemented if it seemed likely that the strong N$ would persist. In particular. Arrfield need not renew the contracts that permit aviation fuel suppliers to operate from its airports. Arrfield would then be free to create its own fuel sale business, buying fuel in bulk to repleni sh the storage tanks at each of its airports in Norland and then selling it directly to airlines He stated that this would almost certainly enhance Arrfield ' s share price

Romuald Marek reminded the Board that four of Arrfield ' s six airports are located in Norland and that those airports charge for aeronautical and non-aeronautical services in N$.

The formal merger with Darrell has been negotiated and the legal formalities have been completed. The two company management teams are working on the integration of the two businesses.

You receive an email from Peter Sorchi, the Chief Executive of the merged company:

From: Peter Sorchi, Chief Executive Officer

To: Senior Finance Manager

Subject: Integration of IT and treasury

Hi,

I need you to advise me on a couple of matters. The attached press clipping shows how sensitive this is.

We need to integrate the IT and treasury functions of the former Wodd and Darrell. I thought that it would be a simple matter of identifying the common ground and slimming down both companies’ departments to cover the new entity, but I have the heads of both IT and treasury from each company arguing that their approaches are better for the merged group and that they should take the lead.

Wodd’s Treasurer claims to be an expert in natural hedging of currency risks and Darrell’s argues that her department was highly successful because it makes excellent use of derivatives for hedging. Both agree only on the fact that they cannot work together. I am afraid that I have to agree with them on that and the Board will have the difficult decision of choosing between them.

I have the opposite problem with the IT function. The two Heads of IT are excited to be able to combine their databases and to develop their respective interests in Big Data. They claim that we should retain all of the professional staff in both departments and possibly even expand the merged IT Department beyond that. Given the rationalisation in all of our other functions, I do not think that we can agree to that, but I would hate to throw away a worthwhile opportunity.

Please give me your thoughts on the following:

What approach to hedging is more likely to meet our needs: natural hedging or heavy use of derivatives?

Ignoring hedging, what other factors should we consider in deciding between the two treasurers?

Are the two heads of IT likely to be correct in arguing that we need to retain all existing IT staff in order to exploit synergies in data, particularly opportunities to leverage Big Data?

What would the challenges be in motivating them to reduce their joint staffing levels and how might we deal with these?

Peter

Wodd’s Chairman enters your office:

" I am glad I caught you, I am looking for some advice, but I do not wish to involve your boss at this stage, or any of the other executive directors.

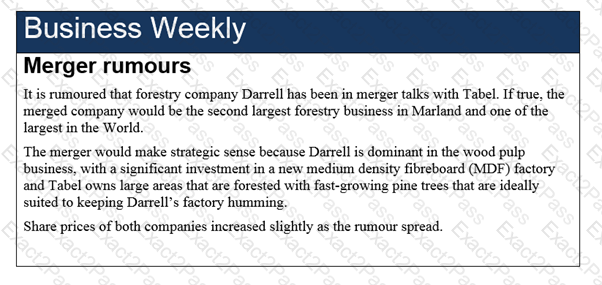

I have been approached by Darrell’s Chairman concerning the possibility of a merger between our two companies. I was a little surprised because it has apparently, according to a press article, been in talks with at least one of our competitors and I suspect that it is keen to merge with any large company that can offer some synergy. I understand that Tabel, another major forestry company, has already rejected its proposal.

I happen to know that Darrell has invested a little too heavily in its new MDF factory. It is state of the art, but it has to operate at close to full capacity in order to be economic and Darrell just hasn’t got sufficient forestry resources to keep the factory operating at full volume without destroying its own forests.

We are attractive to merge with because we own large forests that can sustain Darrell’s needs. We don’t manufacture MDF ourselves, but we have lots of experience of supplying this market with raw material. We would divert lots of this output to Darrell’s factory. Darrell believes that it would be possible to dominate the MDF industry if it merged with a company such as ourselves. The fact that we were quite liquid at the end of last year also helps, because I understand that Darrell is having a few cash flow problems.

Its Chairman proposes a full merger. This will be achieved by the creation of a new parent company which will acquire existing equity in both companies through an exchange of shares. He and I will head a special nomination committee to select the most suitable Board for the new company and then I will step down from the Board while he continues as Chairman of the new company.

Needless to say, this is all highly confidential.

Do you think that it sounds as if there are potential and achievable synergies between Wodd and Darrell?

Would you regard it as a gross ethical breach to keep this conversation just between the two of us for the time being, without warning your boss, until I have had the chance to negotiate further with my counterpart at Darrell? "

Reference Material: