Last Update 8 hours ago Total Questions : 248

The Financial Reporting content is now fully updated, with all current exam questions added 8 hours ago. Deciding to include F1 practice exam questions in your study plan goes far beyond basic test preparation.

You'll find that our F1 exam questions frequently feature detailed scenarios and practical problem-solving exercises that directly mirror industry challenges. Engaging with these F1 sample sets allows you to effectively manage your time and pace yourself, giving you the ability to finish any Financial Reporting practice test comfortably within the allotted time.

The following information is extracted from QQ ' s statement of financial position at 31 March:

Included in other payables is interest payable of $80,000 at 31 March 20X2 and $73,000 at 31 March 20X1.

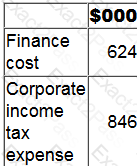

The following information if included within QQ ' s statement of profit or loss for the year ended 31 March 20X2.

Included within finance cost is $124,000 which relates to interest paid on a finance lease. QQ includes finance lease interest within financing activities on its statement of cash flows.

QQ is preparing its statement of cash flows for the year ended 31 March 20X2.

What cash outflow figure should be included for corporate income tax paid within the cash flow from operating activities section of the statement?

Give your answer to the nearest $000.

If an entity makes a capital loss in a period, which of the following is the most likely way that will be allowed for relieving that capital loss?

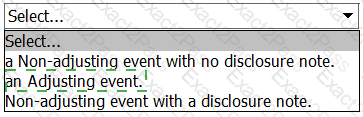

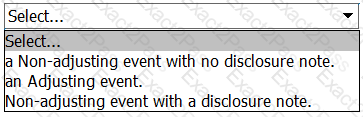

The financial statements of JK for the year ended 31 August 20X4 were approved on 10 November 20X4.

Within these financial statements which of the following would have been treated as a non-adjusting event in accordance with IAS 10 Events After the Reporting Period?

LM received notification on 10 November 20X4 from one of its customers stating they had ceased trading as they had gone into liquidation. The balance outstanding at 31 October 20X4 was $150,000.

In accordance with IAS 10 Events after the Reporting Date this event will be treated as:

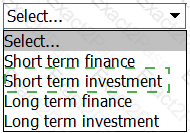

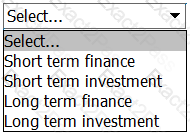

What is the correct classification of a 90-day government bond?

STU commenced trading on 1 January. Total sales for the month of January were $250,000. which were 75% on credit and 25% for cash. Sales are expected to increase by 10% a month Irrecoverable debts are estimated to be 5% of credit sales Of the credit sales expected to pay, 50% pay in the month following the sale and the remaining 50% the month after.

The cash expected to be received in February is:

Which of the following is a characteristic of a defined contribution post-employment benefit scheme?

OP is considering investing in government bonds. The current price of a $100 bond with 8 years to maturity is $88.

The bonds have a coupon rate of 6% and repay face value of $100 at the end of the 8 years.

Calculate the yield to maturity.

Give your answer to one decimal place.

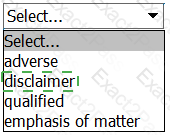

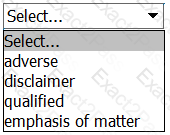

Whilst undertaking an external audit, the auditor has identified that there is insufficient evidence to support the financial statements.

As a result the auditors consider these financial statements to be wholly unreliable for decision making purposes.

This will result in a modified audit report with the opinion being .

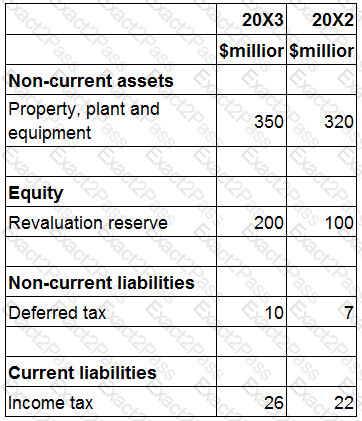

The following information is extracted from the statement of financial position for ZZ at 31 March 20X3:

Included within cost of sales in the statement of profit or loss for the year ended 31 March 20X3 is $20 million relating to the loss on the sale of plant and equipment which had cost $100 million in June 20X1.

Depreciation is charged on all plant and equipment at 25% on a straight line basis with a full year ' s depreciation charged in the year of acquisition and none in the year of sale.

The revaluation reserve relates to the revaluation of ZZ ' s property.

The total depreciation charge for property, plant and equipment in ZZ ' s statement of profit of loss for the year ended 31 March 20X3 is $80 million.

The corporate income tax expense in ZZ ' s statement of profit or loss for year ended 31 March 20X3 is $28 million.

ZZ is preparing its statement of cash flows for the year ended 31 March 20X3.

What figure should be included within cash flows from investing activities for the proceeds of sale of plant and equipment?