Last Update 20 hours ago Total Questions : 392

The Fundamentals of management accounting content is now fully updated, with all current exam questions added 20 hours ago. Deciding to include BA2 practice exam questions in your study plan goes far beyond basic test preparation.

You'll find that our BA2 exam questions frequently feature detailed scenarios and practical problem-solving exercises that directly mirror industry challenges. Engaging with these BA2 sample sets allows you to effectively manage your time and pace yourself, giving you the ability to finish any Fundamentals of management accounting practice test comfortably within the allotted time.

Refer to the exhibit.

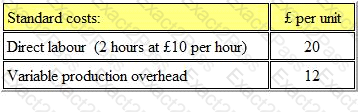

SP, a manufacturing company, uses a standard costing system. The standard variable production overhead cost is based on the following budgeted figures for the year:

During the month of September, 5,300 actual hours were worked and 5,600 standard hours of output were produced. Total variable production overhead costs in September were $8,600.

What was the total variable production overhead variance in September?

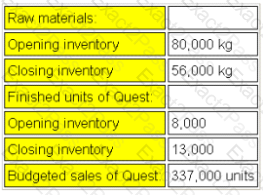

Refer to the exhibit.

Data for October ' s budget for product Quest for the month of October are given below:

Each unit of Quest requires 6kg of raw materials. Strict quality control procedures are applied to the manufacturing process and normal rejection levels are 5% of finished units.

The raw materials purchases budget for the month of October is:

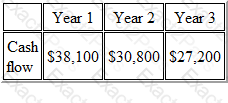

Refer to the Exhibit.

The following forecast cash flows relate to a proposed investment in new delivery vehicles at a total cost of $75,000.

The internal rate of return (IRR) of the proposed investment is (to two decimal places)

Which of the following categories of costs is the most relevant for decision making?

The net present value (NPV) of an investment is as follows.

NPV at 14% = $6,320

NPV at 18% = ($4,600) negative

The internal rate of return (IRR) of the investment is closest to

In an integrated cost and financial accounting system, the accounting entries for the cost of production units completed in the period would be:

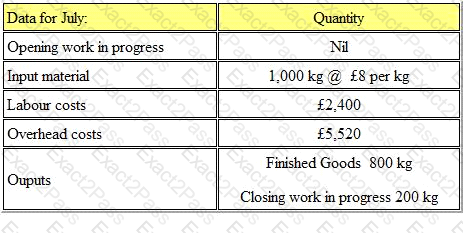

Refer to the exhibit.

The following data refers to a manufacturing process for the month of July:

The work in progress is completed as follows:

(a) 100% for material

(b) 80% for labour

(c) 60% for overhead

What is the value of the finished goods?

Which one of the following is NOT a main purpose of management accounting?

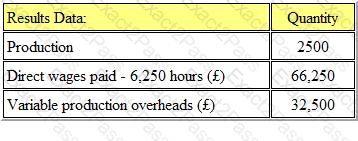

Refer to the exhibit.

A company manufactures a single product, and relevant data is as follows:

Note. Overheads are assumed to be related to direct labor hours.

The actual results for the period were as follows:

What is the variable overhead efficiency variance?

Which of the following best describes a step cost?