We have coached hundreds of senior management accountants, corporate treasury analysts, and strategic finance directors through this final, high-stakes financial tier of the professional qualification. Let's look closely at the modern corporate governance training landscape. The candidates who stumble on this advanced-level evaluation are almost always those who relied on low-tier test pools—those flat, context-stripped answer repositories floating around unverified accounting forums. Those static, unverified materials simply cannot prepare you for the complex real-world investment appraisals or the multi-layered risk management trade-offs tested on the real exam. At Exact2Pass, our approach targets the underlying structural logic, capital frameworks, and risk-mitigation lifecycles of the active CIMA body of knowledge instead. Our F3 exam questions prep delivers comprehensive methodological breakdowns for every capital structure calculation and corporate restructuring scenario. You will master actual core treasury allocations instead of leaning on short-sighted memorization shortcuts. We map out Modigliani-Miller dividend irrelevance proofs, expected value decision trees, business valuation modeling methodologies, and currency swap mechanics step by step. Our learning material is built from the ground up by active Chief Financial Officers and chartered management architects who orchestrate multi-million dollar corporate strategies daily. Because of that, we completely avoid mindless, repetitive question-and-answer lists. Instead, our workspace functions as an active training simulation that forces you to evaluate corporate performance, optimal capital blend limits, and risk thresholds like a principal financial controller. You will learn the exact reason why a specific capital allocation choice or derivative hedging policy succeeds or violates corporate compliance rules. That is how you build real confidence before logging into your official Pearson VUE dashboard to clear this objective test. Our adaptive training software develops deep, practical fiscal skills that transfer perfectly to live boardrooms, helping you pass on your very first try.

Listed Company A has prepared a valuation of an unlisted company. Company B. to achieve vertical integration Company A is intending to acquire a controlling interest in the equity of Company B and therefore wants to value only the equity of Company B.

The assistant accountant of Company A has prepared the following valuation of Company B ' s equity using the dividend valuation model (DVM):

Where:

• S2 million is Company B ' s most recent dividend

• 5% is Company B ' s average dividend growth rate over the last 5 years

• 10% is a cost of equity calculated using the capital asset pricing model (CAPM), based on the industry average beta factor

Which THREE of the following are valid criticisms of the valuation of Company B ' s equity prepared by the assistant accountant?

Company A plans to acquire a minority stake in Company B.

The last available share price for Company B was $0.60.

Relevant data about Company B is as follows:

• A dividend per share of $0.08 has just been paid

• Dividend growth is expected to be 2%

• Earnings growth is expected to be 4%

• The cost of equity is 15%

• The weighted average cost of capital is 13%

Using the dividend growth model, what would be the expected change in share price?

When valuing an unlisted company, a P/E ratio for a similar listed company may be used but adjustments to the P/E ratio may be necessary.

Which THREE of the following factors would justify a reduction in the proxy p/e ratio before use?

Which three of the following are most likely be primary objectives for a newly established, unincorporated entity in the service sector?

The Board of Directors of a small listed company engaged in exploration are currently considering the future dividend policy of the company. Exploration is considered a high-risk business and consequently the company has a low level of debt finance.

Forecasts indicate a period of profit fluctuation in the next few years as the company is planning to embark on a major capital investment project. Debt finance is unlikely to be available due to the project ' s high business risk.

Which THREE of the following are practical considerations when determining the company ' s dividend/retention policy?

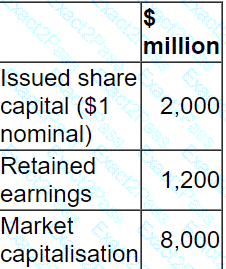

A listed company is financed by debt and equity.

If it increases the proportion of debt in its capital structure it would be in danger of breaching a debt covenant imposed by one of its lenders.

The following data is relevant:

The company now requires $800 million additional funding for a major expansion programme.

Which of the following is the most appropriate as a source of finance for this expansion programme?

XCV can borrow at either 9.5% fixed or the risk-free rate plus 1.3%.

XCV wishes to borrow at a variable rate and thinks that a swap may enable it to do so cheaply

BNM can borrow the same principal sum as XCV It can borrow at 10 5% fixed or the risk-free rate plus 2 1 % BNM wishes to raise fixed rate debt

XCV and BNM have agreed to use an interest rate swap They will share any savings equally

Calculate the effective swap rate that will be paid by XCV.

Give your answer to one decimal place.

The value of a call option will increase because of:

A company ' s current profit before interest and taxation is $1.1 million and it is expected to remain constant for the foreseeable future.

The company has 4 million shares in issue on which the earnings yield is currently 10%. It also has a $2 million bond in issue with a fixed interest rate of 5%.

The corporate income tax rate is 20% and is expected to remain unchanged.

Which of the following is the best estimate of the current share price?

A company is based in Country Y whose functional currency is YS. It has an investment in Country Z whose functional currency is ZS This year the company expects to generate ZS20 million profit after tax.

Tax Regime

• Corporate income tax rate in Country Y is 60%

• Corporate income tax rate in Country Z Is 30%

• Full double tax relief is available

Assume an exchange rate of YS1 = ZS5

What is the expected profit after tax in YS if the ZS profit is remitted to Country Y?