Last Update 21 hours ago Total Questions : 392

The Fundamentals of management accounting content is now fully updated, with all current exam questions added 21 hours ago. Deciding to include BA2 practice exam questions in your study plan goes far beyond basic test preparation.

You'll find that our BA2 exam questions frequently feature detailed scenarios and practical problem-solving exercises that directly mirror industry challenges. Engaging with these BA2 sample sets allows you to effectively manage your time and pace yourself, giving you the ability to finish any Fundamentals of management accounting practice test comfortably within the allotted time.

In the process account, the accounting treatment of the value of the abnormal gain is:

The standard labour hours for all products manufactured by a company include an allowance for idle time. Idle time is budgeted to be 5% of total hours worked. Each unit of product G requires an input of 9.5 active labour hours. The labour rate is $12 per hour.

The standard labour cost shown on the standard cost card for one unit of product G will be

Which THREE of the following cost items would normally be classified as fixed costs?

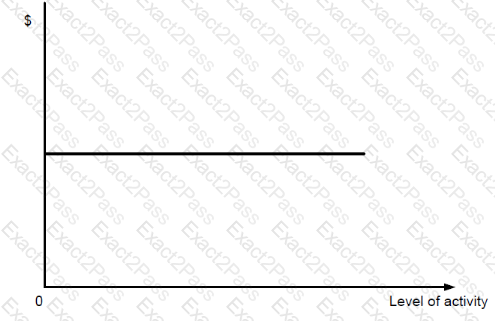

Refer to the exhibit.

Which ONE of the following can be represented by this graph?

Overhead allocation is best described as:

The variable cost of a product is £7 per unit. The fixed costs of the product are £140,000. The break-even point is 70,000 units.

The selling price of the product is:

Give your answer to 2 decimal places.

Normal loss which has a scrap value in a process should be valued at:

Refer to the exhibit.

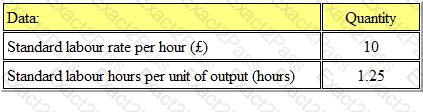

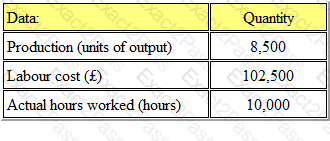

The following standard cost information relates to the production department of BE Ltd.

The actual data for the month of March was as follows:

What is the direct labour efficiency variance (to the nearest whole number)?

Which THREE of the following statements could explain why an adverse labour efficiency variance has arisen?

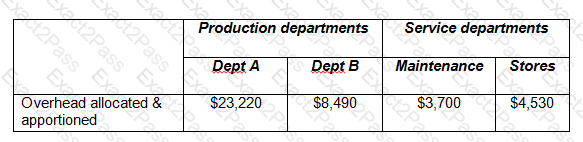

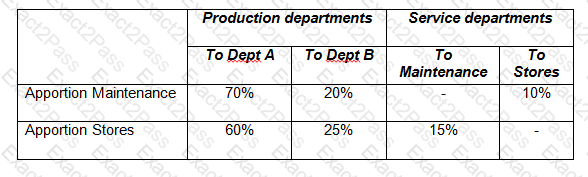

Refer to the exhibit.

The management accountant has completed the initial allocation and apportionment of overheads as follows.

The service department costs are now to be reapportioned to the other departments as follows, taking account of reciprocal servicing.

After the service department costs have been reapportioned, the total overhead cost of Department A, to the nearest $, will be: