Last Update 12 hours ago Total Questions : 1259

The Chartered Wealth Manager (CWM) Certification Level II Examination content is now fully updated, with all current exam questions added 12 hours ago. Deciding to include CWM_LEVEL_2 practice exam questions in your study plan goes far beyond basic test preparation.

You'll find that our CWM_LEVEL_2 exam questions frequently feature detailed scenarios and practical problem-solving exercises that directly mirror industry challenges. Engaging with these CWM_LEVEL_2 sample sets allows you to effectively manage your time and pace yourself, giving you the ability to finish any Chartered Wealth Manager (CWM) Certification Level II Examination practice test comfortably within the allotted time.

Section C (4 Mark)

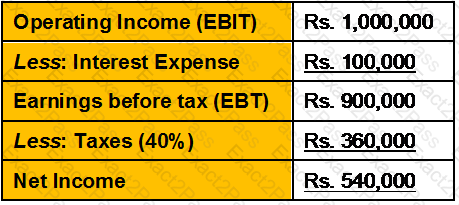

Blair Company has Rs5 million in total assets. The company’s assets are financed with Rs1 million of debt, and Rs4 million of common equity. The company’s income statement is summarized below:

The company wants to increase its assets by Rs1 million, and it plans to finance this increase by issuing Rs1 million in new debt. This action will double the company’s interest expense, but its operating income will remain at 20 percent of its total assets, and its average tax rate will remain at 40 percent. If the company takes this action, which of the following will occur?

Section A (1 Mark)

Which of the following is a special human trait that we need to sharpen and use very often in CRM?

Section B (2 Mark)

Markets would be inefficient if irrational investors __________ and actions of arbitragers were __________.

Section B (2 Mark)

Eric, who has lived in the Netherlands for the whole of his life, arrives in the UK on 1 June 2011 and remains in the UK until 31 December 2011, when he returns permanently to the Netherlands. His UK residence status for 2011-12 is:

Section B (2 Mark)

Withholding Tax Rates for payments made to Non-Residents are determined by the Finance Act passed by the Parliament for various years. The current rates for Interest are:

Section B (2 Mark)

Narayan expects to receive Rs 25000 in net receipts each year for five year and to sell the property for Rs 350,000 at the end of the five-year period, if Narayan expects a 15% return, what would be the value of the property?

Section C (4 Mark)

Read the senario and answer to the question.

Assuming that Mahesh owns a building which he insures along with its contents for Rs. 12 lakh. However the market value of the building and its content is Rs. 15 lakh. Assuming that the building along with its contents is partially destroyed by fire and the loss assessed of Rs. 1 lakh what is the amount of money insurance company would pay as claim reimbursement to Mahesh?

Section A (1 Mark)

After buying two stocks, one rises by 25% an d the other drops by 25%. You congratulate yourself on your brilliance for the first stock and blame bad luck on the second. You are demonstrating which investor bias?

Section B (2 Mark)

Total income of an individual including long-term capital gain of Rs. 50,000/- is Rs.1,60,000/-, the tax on total income for the assessment year 2012-13 shall be: CII-12-13: 852,11-12: 785,10-11:711]

Section B (2 Mark)

Mr. Dinesh is aged 35 years and has a wife aged 30 years old and two small children. His parents are also dependent on him and has a house against which he has taken a housing loan. What is the most important insurance cover required by him at this stage?

Section C (4 Mark)

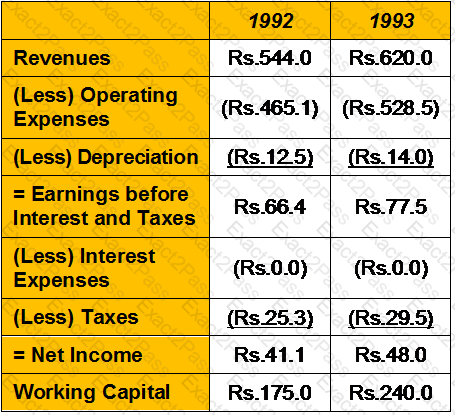

Dab Ltd manufactures, markets, and services automated teller machines. The following are selected numbers from the financial statements for 1992 and 1993 (in millions):

The firm had capital expenditures of Rs15 million in 1992 and Rs18 million in 1993. The working capital in 1991 was Rs180 million.

Estimate the cash flows to equity in 1992 and 1993. (in Rs Millions)

Section B (2 Mark)

Which one of the above statements is/are correct?

Section A (1 Mark)

The cost which the Wealth management firms would generally not be able to fully absorb the revenue shock in the near future is known as Sticky Cost.

Section B (2 Mark)

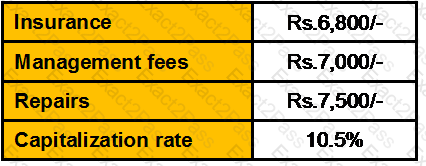

Mahesh wants to sell a property for Rs. 30 lakhs. He is earning rent from tenant Rs. 3,60,000. He is spending following amounts annually on that property

Based on the above information what should be the value of the property would be:

Section C (4 Mark)

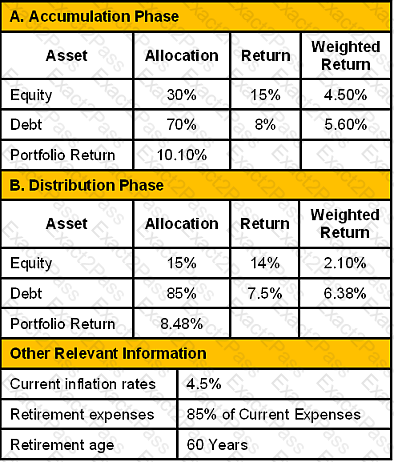

Mr. Raman Gehlot, aged 55 years, is owner of midsized business firm. His family consists of his wife Anupama, aged 55, son Nishant aged 29 and daughter Nivedita aged 27. His wife is a housewife and social worker. Both of their children are happily married and well settled. The couple anticipates their life expectancy to be 75 years each.

The gross annual income of Raman for the previous year 2010–11 is expected to be Rs. 9,60,000. The couples’ household expenses are estimated to be Rs. 4,90,000 p.a. Taking into account incidental expenses of another Rs. 85,000 the net expenses of the family are estimated to be Rs. 5,75,000 for the previous year 2010–11. Thus they achieved a net surplus of Rs. 3,85,000 during the year. Raman has a net saving of Rs. 12,00,000 which he would like to invest for his post retirement purposes at the beginning of the year.

Currently Raman has approximately 5 years left for retirement and thus he is not very aggressive in his investments. The returns of his portfolio based on asset allocation during the accumulation and distribution phase are calculated as below:

Section C (4 Mark)

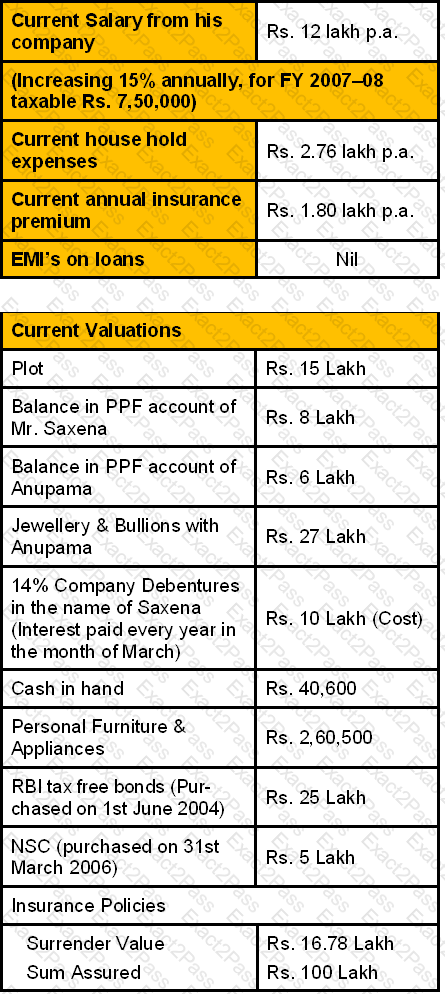

Mr. Saxena, age 45 years, is a software engineer and promoter of an Indian MNC. His family comprises his wife Anupama, age 43 years, who is a house wife, elder son Arup, 16 years (studying in 10th standard) and daughter Aarti, 14 years (studying in 8th standard). The family resides in their self owned residential house in Mumbai. Most of their life amenities such as cars, abroad vacations and full education cost of both kids are provided by Mr. Saxena’s company, as he is the Managing Director of his company. The company is growing consistently and is on way to become a global legend in its field of operations. As such the future prospects of Mr. Saxena are generous and progressive.

Mr. Saxena, age 45 years, is a software engineer and promoter of an Indian MNC. His family comprises his wife Anupama, age 43 years, who is a house wife, elder son Arup, 16 years (studying in 10th standard) and daughter Aarti, 14 years (studying in 8th standard). The family resides in their self owned residential house in Mumbai. Most of their life amenities such as cars, abroad vacations and full education cost of both kids are provided by Mr. Saxena’s company, as he is the Managing Director of his company. The company is growing consistently and is on way to become a global legend in its field of operations. As such the future prospects of Mr. Saxena are generous and progressive.

Mr. Saxena is now planning to allocate his resources in the right fashion with your help as a Chartered Wealth Manager.

For this, he has disclosed his current personal financial details as follows:

Other details for FY 2007–08

1. Mr. Saxena has made investments worth Rs. 1.50 Lakh qualified U/S 80C.

2. He has donated Rs. 50,000 to Prime Ministers National Relief Fund.

3. He has transferred interest received by him on debentures to his wife’s bank account the same date he received it.

4. Mr. Saxena’s minor son, Arup, is a recognized child artist in children cinema and documentary films. Arup earned a sum of Rs. 1,50,000 from his assignments.

Mr. Saxena wants to resolve all estate bequeathing matters in his life time so that there should be no dispute after his death. For this purpose he has prepared a “Holograph Will”.

Current estimates of economy are positive and interest rates are not likely to increase further in near future. The family has a health cover provided by the company of Mr. Saxena. Also his house with all its contents is insured adequately.

Section A (1 Mark)

Which ONE of the following in not the requirement for managing customer?

Section A (1 Mark)

The strategies of convertible arbitrage, emerging markets, equity market neutral and fixed income arbitrage are categories of which alternative investments class?

Section A (1 Mark)

Supporting customers through the process of selecting, purchasing, and maintaining a product or service is known as:

Section B (2 Mark)

Rakhi purchased a piece of land on 25-4-1979 for Rs.80000. This land was sold by him on 23-12-2011 for Rs.1250000. The market value of the land as on 1-4-1981 was Rs.98000. Expenses on transfer were 1.5% of the sale price. Compute the capital gain for the assessment year 2012-13. [CII-12-13: 852,11-12: 785,10-11:711]

Section C (4 Mark)

Read the senario and answer to the question.

Saxena wants to know his income tax liability for FY 2007–08 without taking into consideration any interest income from NSC. Calculate the same including surcharge and Educational Cess.

Section A (1 Mark)

To take care of the risks during the foreign travel, Overseas Travel Insurance policy cover provides various other covers, in addition to __________ insurance, such as baggage cover, loss of transport cover, personal accident cover, personal legal liability cover etc.

Section A (1 Mark)

Deduction under section 80-IC is allowed to the extent of:

Section C (4 Mark)

Suppose ABC Ltd. is trading at Rs. 4457 in June. An investor Mr. A buys a Rs 4500 call for Rs. 100 while shorting the stock at Rs. 4457. The net credit to the investor is Rs. 4357

What would be the Net Payoff of the Strategy?

• If ABC Ltd closes at 4145

• If ABC Ltd closes at 4983

Section C (4 Mark)

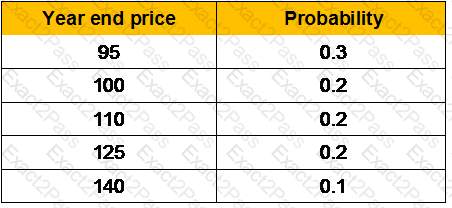

A share pays nil dividend and its current market price is Rs.100. The possible selling prices at the end of a year and the probabilities are:

What is the expected rate of return at the end of the year?

Section A (1 Mark)

The following is capital receipt:

Section A (1 Mark)

As per ARTICLE 12 in DTTA with US , the maximum tax rate on the gross amount of the royalties or fees for included services in the Article is:

Section A (1 Mark)

Garima deposits Rs. 2,000/- every month in an account and is getting interest @ 12 % per annum compounded monthly. How much will be her nest egg after 10 years ?

Section B (2 Mark)

Which of the following are the two skills associated with being a good listener?

Section B (2 Mark)

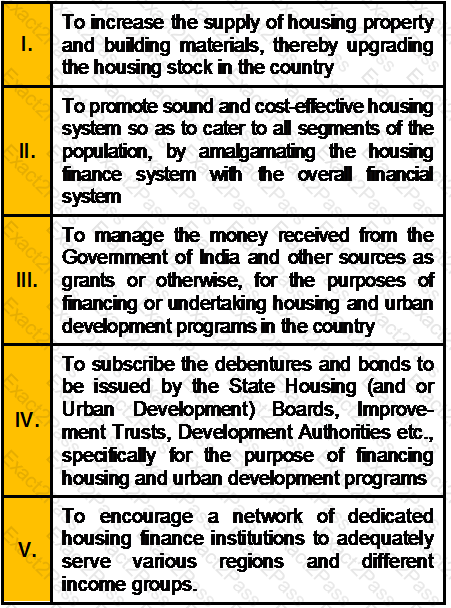

Which of the following are the objectives of National Housing Bank in Indian Real Estate Market?

Section B (2 Mark)

Which of the following is an inferential data (i.e. data which may not be correctly obtained by simply asking a direct question)?

Section C (4 Mark)

Mr. Rajesh Rawat deposits Rs. 15,000 per month at the end of the month for 6.50 years in an account that pays a ROI of 8.80% per annum compounded quarterly. What will be the amount in the account after 6.50 years?

Section A (1 Mark)

The fact that a consumer feels a strong moral and ethical responsibility to repay a loan on time refers to the ______________________ of that individual.

Section A (1 Mark)

A general theoretical perspective in social psychology concerned with the issue of social perception. is known as_____________

Section C (4 Mark)

Read the senario and answer to the question.

Whether Mrs. Deepika as a resident individual can invest in units of Mutual Funds, Venture Funds, and Promissory notes without opening the bank account in foreign country?

Section A (1 Mark)

Financial Independence usually occurs between _______

Section A (1 Mark)

Land plus anything permanently fixed on it, including building, sheds and other items attached to the structure refers to _____.

Section A (1 Mark)

A(n) _________________________ combines a normal debt instrument with a credit option. It allows the issuer of the debt instrument to lower its loan repayments if some significant factor changes.

Section A (1 Mark)

Accumulation, preservation and distribution are stages of

Section B (2 Mark)

The term “permanent establishment” includes especially:

Section A (1 Mark)

In US which of the following is classified as passive income?

Section A (1 Mark)

Debt investments in real estate, such as mortgages or deeds of trust, are called income property investments.

Section C (4 Mark)

Read the senario and answer to the question.

Assume Reena retires at the age of 60 years and invests her salary at 8% p.a.What will be the future value of Reena’s salary at the time of her retirement if she saves her entire salary?

Section A (1 Mark)

Credit reports provided by credit bureaus provide lenders:

Section B (2 Mark)

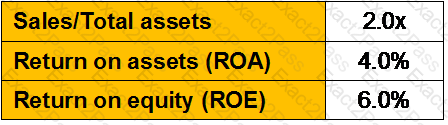

The Wilson Corporation has the following relationships:

What is Wilson’s profit margin and debt ratio?

Section C (4 Mark)

At end of this year ICICI Ltd. will pay a dividend on its stock of Rs. 5 per share. The dividend is expected to remain same for next year. During third year dividend is expected to be Rs.6 from there on, the dividend is expected to grow at 5% per year indefinitely. Stocks with similar risk are currently priced to provide a 10% expected return. What is the intrinsic value of ICICI Ltd.

Section C (4 Mark)

Read the senario and answer to the question.

You have reviewed the investments of Nimita for the purview of retirement. You advise that a balance be restored from risk perspective and accordingly Rs. 15 lakh be shifted to a Debt MF scheme. You advise to further start SIPs immediately in the ratio of 60:40 in the newly started debt MF scheme and the existing Equity MF scheme for the next 21 years to accumulate a corpus so that the same sustains for the next 25 years if invested in an investment instrument yielding 7.50%. What approximate amount of SIPs should be made in Debt and Equity MF schemes?

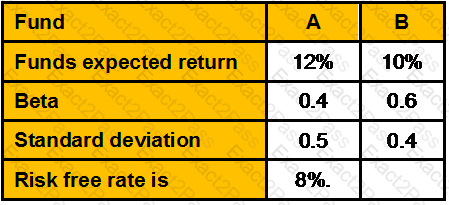

Section B (2 Mark)

The following parameters are available for two mutual funds:

Calculate Treynor’s performance index for Fund A & Fund B respectively

Section A (1 Mark)

A well-diversified portfolio is defined as

Section A (1 Mark)

In a life insurance contract, offer refers to