Last Update 6 hours ago Total Questions : 268

The F2 Advanced Financial Reporting content is now fully updated, with all current exam questions added 6 hours ago. Deciding to include F2 practice exam questions in your study plan goes far beyond basic test preparation.

You'll find that our F2 exam questions frequently feature detailed scenarios and practical problem-solving exercises that directly mirror industry challenges. Engaging with these F2 sample sets allows you to effectively manage your time and pace yourself, giving you the ability to finish any F2 Advanced Financial Reporting practice test comfortably within the allotted time.

HJ is currently in dispute with an employee, who is claiming $400,000 in a legal case against them.

HJ ' s legal advisors have stated that it is probable that they will lose the case and will have to pay the amount claimed.

Also, HJ are claiming $250,000 from a supplier of defective goods and the legal advisors have stated that it is probable that HJ will be successful in this claim.

What is the correct accounting treatment for these two items in HJ ' s financial statements?

XYZ had 600,000 ordinary shares in issue on 1 July 20X4. On 1 January 20X5, the entity made a 1 for 2 bonus issue. The profit attributable to ordinary shareholders for the year ended 30 June 20X5 was $2,925,000.

What is the basic earnings per share for the year ended 30 June 20X5?

Which of the following, in accordance with IFRS 2 Share-based Payments, are only applicable to the accounting treatment of cash settled rather than equity settled share-based payment schemes?

Select ALL that apply.

RS has issued an instrument with a nominal value of $1 million, at a discount of 2.5%, and a coupon rate of 6%. The terms of the issue are that the instrument must either be redeemed at par, at the option of the holder, in three years ' time, or alternatively converted into equity shares in RS.

The characteristics of this instrument taken as a whole indicates that it would be classifed as which of the following?

RST sells computer equipment and prepares its financial statements to 31 December.

On 30 September 20X5 RST sold computer software along with a two year maintenance package to a customer. The customer is given the right to return the goods within six months and claim a full refund if they are not satisfied with the computer software. The risk of return is considered to be insignificant for RST.

How should the revenue from this transaction and the right of return be recognised in the financial statements for the year ended 31 December 20X5?

The dividend yield of ST has fallen in the year to 31 May 20X5, compared to the previous year.

The share price on 31 May 20X4 was $4.50 and on 31 May 20X5 was $4.00. There were no issues of share capital during the year.

Which of the following should explain the reduction in the dividend yield for the year to 31 May 20X5 compared to the previous year?

ST acquired 75% of the 2 million $1 equity shares of CD on 1 January 20X3, when the retained earnings of CD were S3,550,000. CD has no other reserves.

ST paid $5,600,000 for the shares in CD and the non controlling interest was measured at its fair value of S1,400,000 at acquisition.

At 1 January 20X3, the fair value of CD ' s net assets were equal to their carrying amount, with the exception of a building. This building had a fair value of $1,000,000 in excess of its carrying amount and a remaining useful life of 25 years on 1 January 20X3.

At 31 December 20X5, the retained earnings of ST and CD were $8,500,000 and $5,250,000 respectively.

What is the figure for non-controlling interest to be shown in the consolidated statement of financial position of ST as at 31 December 20X5?

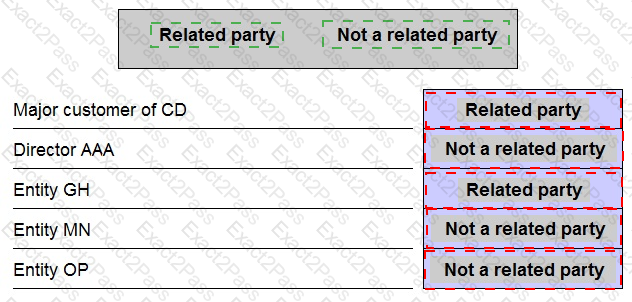

AAA is the only director of entity CD. AAA is also a director of entity GH. CD owns 30% of the equity of MN and 60% of the equity of OP.

Identify which of the following are related parties of CD by placing the appropriate response against one.

As at 31 October 20X7 TU ' s financial statements show the entity having profit after tax of $600,000 and 900,000 $1 ordinary shares in issue. There have been no issues of shares during the year. At 31 October 20X7 TU have 300,000 share options in issue, which allow the holders to purchase ordinary shares at $2 a share in 3 years ' time. The average price of the ordinary shares throughout the year was $5 a share.

What is the diluted earnings per share for the year ended 31 October 20X7?

GH issued a 6% debenture for $1,000,000 on 1 January 20X4. A broker fee of $50,000 was payable in respect of this issue. The effective interest rate associated with this debt instrument is 7.2%.

The carrying value of the debenture at 31 December 20X4 is: