Last Update 6 hours ago Total Questions : 268

The F2 Advanced Financial Reporting content is now fully updated, with all current exam questions added 6 hours ago. Deciding to include F2 practice exam questions in your study plan goes far beyond basic test preparation.

You'll find that our F2 exam questions frequently feature detailed scenarios and practical problem-solving exercises that directly mirror industry challenges. Engaging with these F2 sample sets allows you to effectively manage your time and pace yourself, giving you the ability to finish any F2 Advanced Financial Reporting practice test comfortably within the allotted time.

On 1 January 20X7 GH purchased plant and equipment at a cost of $400,000. The temporary differences in respect of this plant and equipment at 31 December 20X7 and 20X8 have been calculated as follows:

Assume that there are no other temporary differences in the periods and that the corporate income tax rate is 25%. GH is expected to have significant taxable profits in the future.

Which of the following is the correct impact in GH ' s statement of financial position at 31 December 20X8 in respect of deferred tax?

ST acquired 80% of the equity shares of AB on 1 January 20X7. AB acquired 60% of the equity shares of UV on 1 January 20X8. Profit for the year ended 31 December 20X9 for AB is $160,000 and for UV is $100,000.

Calculate the non-controlling interest figure to be included within ST ' s consolidated statement of profit or loss for the year ended 31 December 20X9.

Give your answer to the nearest whole number in $000s.

$ ?

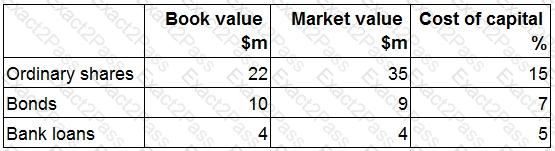

The capital structure of ST is summarised in the table below:

What is the weighted average cost of capital of ST?

Give your answer as a percentage to one decimal place.

? %

CD granted 1,000 share options to its 100 employees on 1 January 20X8.To be eligible, employees must remain employed for 3 years from the grant date. In the year to 31 December 20X8, 15 staff left and a further 25 were expected to leave over the following two years.

The fair value of each option at 1 January 20X8 was $10 and at 31 December 20X8 was $15.

Which THREE of the following are true in respect of recording these share options in the year ended 31 December 20X8?

Taking each statement individually, which of the following explains the movement in the gross profit margin from 20X4 to 20X5 as calculated by the analysts?

Which of the following is NOT an example of an unconsolidated structured entity as defined in IFRS12 Disclosure of Interests in Other Entities?

Following the impairment review of the investment in BC, what would be the carrying value of this associate in KL ' s consolidated statement of financial position at 31 December 20X9?

ST has in issue unquoted 7% debentures which were issued at par and are redeemable in 1 year ' s time. These debentures cannot be traded. The yield to maturity on these debentures has been calculated at 5%.

Which of the following would explain why the yield to maturity is lower than the coupon?

AB sold the majority of its operating equipment to LM for cash on 30 December 20X9 and then immediately leased it back under an operating lease.

AB used the cash proceeds from the sale to reduce its long term borrowings significantly. No early repayment charge was levied by the lender.

Which of the following statements is true in respect of AB ' s ratios calculated at 31 December 20X9?

Which TWO of the following are TRUE in respect of preparing a consolidated statement of cash flows where there has been an acquisition of a subsidiary part way through the year?