Last Update 5 hours ago Total Questions : 260

The Management Accounting content is now fully updated, with all current exam questions added 5 hours ago. Deciding to include P1 practice exam questions in your study plan goes far beyond basic test preparation.

You'll find that our P1 exam questions frequently feature detailed scenarios and practical problem-solving exercises that directly mirror industry challenges. Engaging with these P1 sample sets allows you to effectively manage your time and pace yourself, giving you the ability to finish any Management Accounting practice test comfortably within the allotted time.

A manager in your organisation says, " I have spare capacity and I need a unit cost as a basis for pricing a special one-off contract. You have provided me with a relevant cost of $6.50 per unit and a full production cost of $8.00 per unit. Please explain which unit cost I should use. "

Which cost should be used in this decision and why?

Which of the following, regarding costing methods, is true?

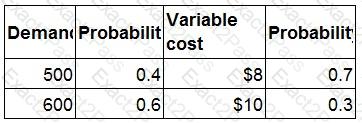

A company is launching a new product with a selling price of $20.

Demand and variable cost are both uncertain and possible demand levels and variable costs are given below:

Outcomes for demand and variable cost are independent.

What is the expected contribution from the product?

Give your answer as a whole number.

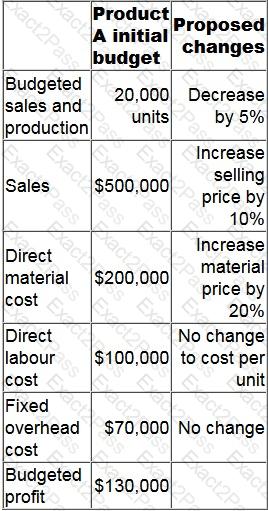

Company M is preparing its budgeted profit statement for the next year.

The initial budget for Product A is as follows with some changes proposed by the sales director to increase the quality of the product.

What would the budgeted profit of Product A be if the proposed changes are made?

Give your answer as a whole number.

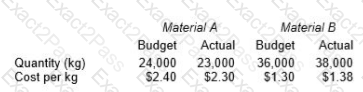

A company produces a product that requires two materials, Material A and Material B. Details of the material quantities and costs for August are given in the table below.

Budgeted and actual output of the product for August was 12,000 units.

The material mix variance for August is:

Select the benefits to a company of using sensitivity analysis in investment appraisal.

(Select all the true statements.)

How would the cost of recycling scrap be classified in an environmental costing system?

The budgetary control report of XYZ for the latest period is shown below. Variances in brackets are adverse.

What is the sales volume profit variance?

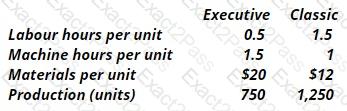

D3 makes 2 types of toilets - the Executive (Ex) and the Classic (CI). Direct labour costs $6 per hr and overheads are absorbed on a machine hour basis. The overhead absorption rate for the period is $28 per machine hour. What is the traditional cost per unit for (Ex) and (CI)?

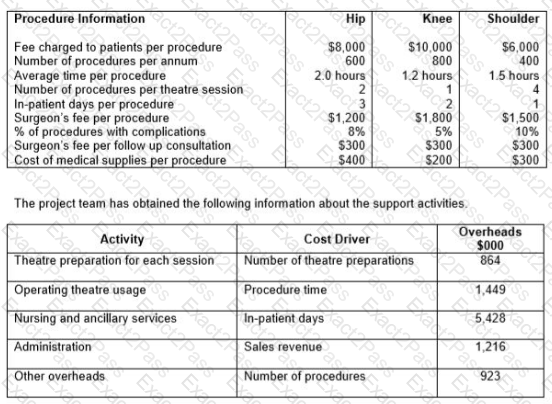

A healthcare company specializes in hip, knee and shoulder replacement operations, known as surgical procedures. As well as providing these surgical procedures the company offers pre operation and post operation in-patient care, in a fully equipped hospital, for those patients who will be undergoing the surgical procedures.

Surgeons are paid a fixed fee for each surgical procedure they perform and an additional amount for any follow-up consultations. Post procedure follow-up consultations are only undertaken if there are any complications in relation to the surgical procedure. There is no additional fee charged to patients for any follow up consultations. All other staff are paid annual salaries.

The company’s existing costing system uses a single overhead rate, based on revenue, to charge the costs of support activities to the procedures. Concern has been raised about the inaccuracy of procedure costs and the company’s accountant has initiated a project to implement an activity-based costing (ABC) system. The project team has collected the following data on each of the procedures.

Calculate the profit per procedure for each of the three procedures using activity-based costing.

What was the profit for the knee procedure, using ABC costing?