Last Update 9 hours ago Total Questions : 248

The Financial Reporting content is now fully updated, with all current exam questions added 9 hours ago. Deciding to include F1 practice exam questions in your study plan goes far beyond basic test preparation.

You'll find that our F1 exam questions frequently feature detailed scenarios and practical problem-solving exercises that directly mirror industry challenges. Engaging with these F1 sample sets allows you to effectively manage your time and pace yourself, giving you the ability to finish any Financial Reporting practice test comfortably within the allotted time.

Which TWO of the following would improve a company ' s short term cash flow position?

Which THREE of the following must an auditor consider in order to form an opinion on the truth and fairness of an entity ' s financial statements?

Which of the following is an example of a progressive tax?

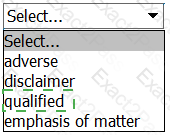

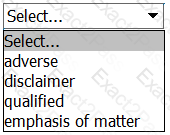

The auditor has identified a material but not pervasive mis-statement whilst undertaking the external audit of an entity ' s financial statements.

This will result in a modified audit report with the opinion being .

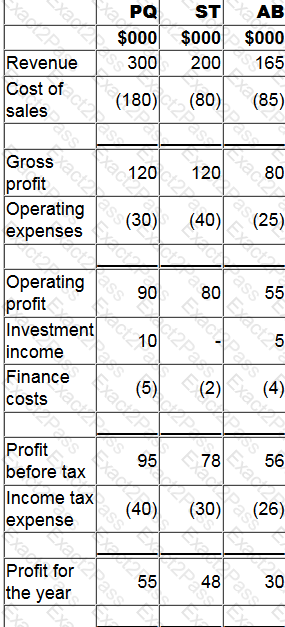

The statement of profit or loss for PQ, ST and AB for the year ended 31 December 20X0 are shown below:

1. PQ acquired 80% of its subsidiary, ST, on 1 January 20X0 and 40% of its associate, AB, on 1 September 20X0.

2. Since acquistion PQ has sold goods to ST and AB for $20,000 and $30,000 respectively. At the year end both ST and AB have 50% of these goods remaining in inventory. PQ uses a mark-up of 20% on all of its sales.

3. Since acquisition the goodwill in respect of ST has been impaired by $8,000 and the investment in AB has been impaired by $2,000.

4. PQ uses the fair value method for non-controlling interest at acquisition.

Calculate the amount that will be shown as the share of profit of associate in PQ ' s consolidated statement of profit or loss for the year ended 31 December 20X0.

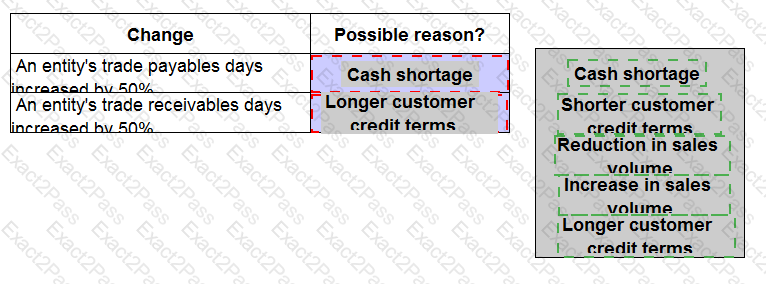

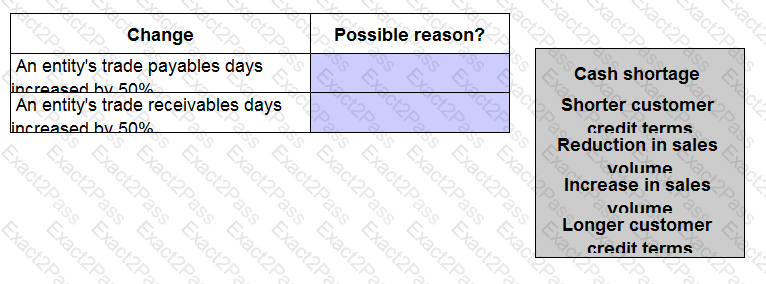

Indicate the possible reasons for the changes identified below to working capital ratios by placing the appropriate reason against each change.

An entity had a current tax liability of $187,000 in its statement of financial position as at 30 September 20X5. It was subsequently negotiated and eventually agreed with the tax authorities that the entity would pay $192,000 and this was paid on 6 January 20X6.

The entity ' s management estimate that the tax due on profits for the year to 30 September 20X6 is $231,000.

Calculate the entity ' s corporate income tax expense included in its statement of profit or loss for the year ended 30 September 20X6.

Give your answer to the nearest whole $000.

There are two main approaches to corporate governance: rules-based and principle-based.

Which THREE of the following are correct?

BCD owns an item of plant which cost $20,000 and at the time of purchase was assessed to have a useful economic life of 8 years and a residual value of $2,000

The carrying amount of the plant at 1 January 20X8 is $11,000. On that date BCD ' s directors estimate that the plant ' s remaining useful life is now 6 years The residual value remains unchanged at $2,000

What is the depreciation charge for this plant for the year ended 31 December 20X8?

Give your answer to the nearest $.

Country A permits the following deductions in an entity ' s annual corporate income tax return in relation to entertaining expenses and gifts;

1 Employee entertaining up to a value of $150 a head

2 Entertaining of overseas customers.

3 Individual gifts not to exceed $10 in value

Which THREE of the following actions would be regarded as tax evasion?