Last Update 7 hours ago Total Questions : 248

The Financial Reporting content is now fully updated, with all current exam questions added 7 hours ago. Deciding to include F1 practice exam questions in your study plan goes far beyond basic test preparation.

You'll find that our F1 exam questions frequently feature detailed scenarios and practical problem-solving exercises that directly mirror industry challenges. Engaging with these F1 sample sets allows you to effectively manage your time and pace yourself, giving you the ability to finish any Financial Reporting practice test comfortably within the allotted time.

Which TWO of the following are features of a bank overdraft?

The following information relates to a single asset:

*Original cost of $186,000

*Estimated residual value of $6,000

*Expected useful life of 10 years

*Accumulated depreciation at 31 December 20X5 of $66,960

*Annual depreciation rate of 20% on a reducing balance basis

Calculate the amount of depreciation that should be charged to profit or loss for the year ended 31 December 20X6.

Give your answer to the nearest whole number.

Which of the following is a type of short-term finance?

Which of the following would be classified as a parent and subsidiary relationship in accordance with IFRS 10 Consolidated Financial Statements?

XYZ operates in Country P where the tax rules state entertaining costs and accounting depreciation are disallowable for tax purposes.

In year ending 31 March 20X4, XYZ made an accounting profit of $240,000.

Profit included $14,500 of entertaining costs and $5,000 of income exempt from taxation.

XYZ has plant and machinery with accounting depreciation amounting to $26,300 and tax depreciation amounting to $35,200.

Calculate the taxable profit for the year ended 31 March 20X4.

During the year a piece of equipment that originally cost $96,000, with accumulated depreciation of $39,000, met the criteria of IFRS 5 Non-current Assets Held for Sale and Discontinued Operations to be classified as held for sale.

The equipment is being advertised for sale at $46,000 and costs of $1,000 will be incurred to enable the sale to be completed.

At what value should the equipment be included in the statement of financial position at the year end assuming that it remains unsold?

Give your answer to the nearest whole number.

GH ' s tax liability at 30 June 20X3 in respect of the tax charge on the profits for the year ended 30 June 20X3 is $876,000.

There was an over provision of $105,000 that related to the tax charge on the profits for the year ending 30 June 20X2.

What amount should be shown in GH ' s statement of profit or loss for the year ending 30 June 20X3?

Give your answer to the nearest $.

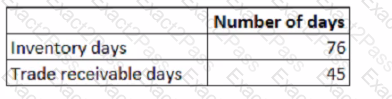

ABC has the following working capital ratios at 31 December 20X2:

During the year ended 31 December 20X4 credit purchases were $1,700,000 and at 31 December 20X4 the outstanding trade payables balance was $340,000

During the year ended 31 December 20X4 credit purchases were $1,700,000 and at 31 December 20X4 the outstanding trade payables balance was $340,000

Calculate the working capital cycle for ABC.

Give your answer to the nearest whole number of days and assume there are 365 days in a year.

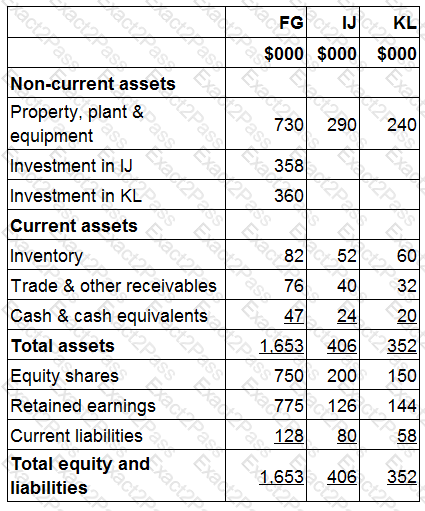

Statements of financial position for FG, IJ and KL at 31 December 20X5 include the following balances:

FG acquired 90% of IJ ' s equity shares for $358,000 on 1 July 20X5 when IJ ' s retained earnings were $98,000.

FG acquired 100% of KL ' s equity shares for $360,000 on 1 January 20X5 when KL ' s retained earnings were $155,000.

FG used the proportion of net assets method to value non-controlling interests at acquisition.

KL sold a piece of land to FG for $130,000 on 1 September 20X5. At the date of transfer the land had a carrying value of $50,000.

The management of FG expect KL to make profits in the future and no impairment ot its goodwill was proposed at 31 December 20X5.

Calculate the total goodwill to be included in FG ' s consolidated statement of financial position as at 31 December 20X5.

Give your answer to the nearest whole $.