Last Update 8 hours ago Total Questions : 248

The Financial Reporting content is now fully updated, with all current exam questions added 8 hours ago. Deciding to include F1 practice exam questions in your study plan goes far beyond basic test preparation.

You'll find that our F1 exam questions frequently feature detailed scenarios and practical problem-solving exercises that directly mirror industry challenges. Engaging with these F1 sample sets allows you to effectively manage your time and pace yourself, giving you the ability to finish any Financial Reporting practice test comfortably within the allotted time.

An entity purchased an asset on 1 April 20X4 for $320,000, exclusive of import duties of $32,000.

The entity sold the asset on 31 March 20X9 for $480,000 incurring legal fees of $12,000.

The entity is resident in Country Y where chargeable capital gains are taxed at 20% and no indexation is allowed.

Calculate the amount of capital tax that the entity is due to pay.

Give your answer to the nearest whole $.

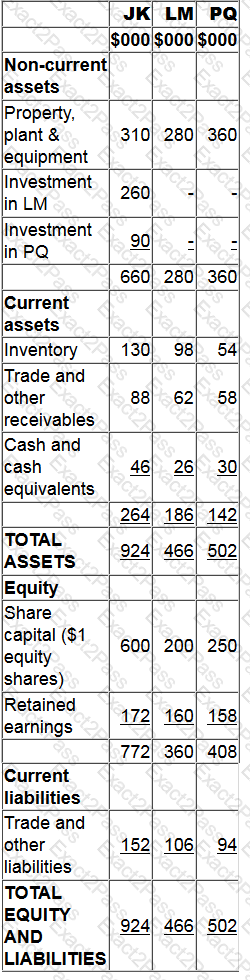

Statements of financial position as at 31 December 20X8 for JK, LM and PQ are as follows:

[1] JK purchased 80% of LM ' s $1 equity shares on 1 January 20X8 for $260,000 when the retained earnings of JK were $110,000. At that date the non-controlling interest had a fair value of $63,000.

[2] JK purchased 25% of PQ ' s $1 equity shares on 1 January 20X8 for $90,000 when the retained earnings of PQ were $96,000.

[3] During the year JK sold goods to LM for $32,000 at a mark up of 33.33% on cost. Half of the goods were still in LM ' s inventory at 31 December 20X8.

[4] LM transferred $32,000 to JK on 30 December 20X8 in settlement of the inter-group trade. JK did not record the cash in its financial records until 2 January 20X9.

Calculate the goodwill arising on the acquisition LM.

Give your answer to the nearest $.

A non-executive director of a company is somebody who:

An entity acquires 100% of the equity shares in another entity.

The consideration paid for the shares is less than the fair value of the net assets acquired.

Which of the following is the correct accounting treatment for the difference between the consideration paid and the fair value of the net assets acquired, in accordance with IFRS 3 Business Combinations?

Which of the following is the most appropriate definition of the term ' factoring ' ?

Company RET ' s financing activities are exactly 35% of their operating activities expenses each month. Below is a list of Company RET ' s total expenses for this month:

Inventory supplies purchased: £145,000

Employee wages: £65,000

Purchase of a shop: £105,000

Dividend payments: ??

Cash repayments on loan: £61,000

What is company RET ' s total dividends payment for this month?

For an incorporated business, the taxation of trading income is a form of direct taxation which is based on:

030d49a3-3c4c-45ad-9aee-710302f219f1: Entities normally pay taxation on their worldwide income in the country in which they are deemed to be resident.

Residency is determined by the

UV ' s financial statements for the year ended 31 March 20X8 were approved for publication on 30 June 20X8.

In accordance with IAS 10 Events After the Reporting Period, which of the following material events would have been classified as a non-adjusting event in these financial statements?

Country X charges corporate income tax at the rate of 20% on all income irrespective of whether it is paid out as a dividend. Country Y charges corporate income tax at the rate of 25% on all income.

An entity, AA, which is resident in Country X pays a dividend of $100,000 to another entity, BB, which is resident in Country Y.

Countries X and Y have a double taxation treaty which adopts the exemption method in respect of this type of transaction.

What is BB ' s liability to tax in Country Y in respect of the dividend income received?