Last Update 9 hours ago Total Questions : 248

The Financial Reporting content is now fully updated, with all current exam questions added 9 hours ago. Deciding to include F1 practice exam questions in your study plan goes far beyond basic test preparation.

You'll find that our F1 exam questions frequently feature detailed scenarios and practical problem-solving exercises that directly mirror industry challenges. Engaging with these F1 sample sets allows you to effectively manage your time and pace yourself, giving you the ability to finish any Financial Reporting practice test comfortably within the allotted time.

Country X levies corporate income tax at a rate of 25% and charges income tax on all profits irrespective of whether they are distributed by way of dividend. Country Y levies corporate income tax at a rate of 20%.

A, who is resident in Country X, pays a divided to B, who is resident in Country Y. B is required to pay corporate income tax on the dividend received from A, but a deduction can be made for the tax suffered on this dividend restricted to a rate of 20%.

Which method of relief for foreign tax does this describe?

XY is an entity incorporated in Country B but operates in several countries. Monthly management meetings to decide on strategic matters take place in Country A, where the majority of its production happens. XY sells most of its goods to Country C.

In accordance with the Organization for Economic Co-operation and Development (OECD) rules on corporate residence which of the following statements is true?

At 31 December 20X4 the directors of MNO decide to revalue its property. Before revaluation adjustments the balances relating to property are as follows:

The property has been revalued at $1,600,000.

How much will be included within MNO ' s statement of financial position at 31 December 20X4 for revaluation surplus?

The subsidiary company of Group XY has purchased £150,00 worth of goods its parent company. However the goods purchased have yet to arrive at the subsidiary at the end of the financial year 20X4, meaning there is

a disagreement in the current account balances between the parent and subsidiary.

With Group XY looking to produce its CSOFP for the end of the financial year, which of the following statements are true in relation to accounting for this disagreement? Select ALL that apply.

Which one of the following is NOT a step in the development of an International Financial Reporting Standard (IFRS)?

The United Kingdom (UK) uses a principle based approach to corporate governance which means:

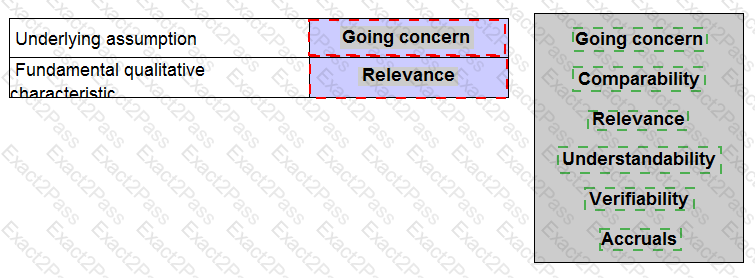

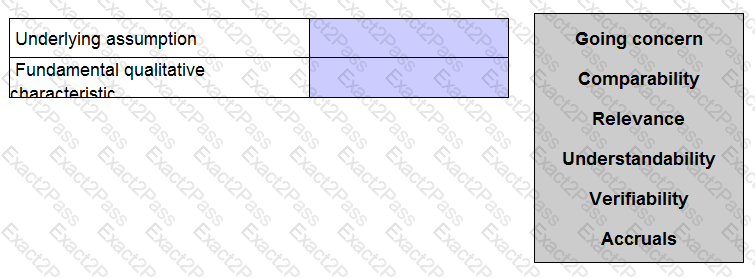

The Conceptual Framework for Financial Reporting issued by the International Accounting Standards Board (known as the IASB ' s conceptual framework) includes one underlying assumption about the preparation of financial statements and two fundamental qualitative characteristics for financial information.

Identify the underlying assumption and one of the fundamental characteristics by placing one of the options in each of the boxes below.

XYZ ' s accounting profit for the last reporting period is $200,000. This is after deduction of:

• Accounting depreciation of $40,000.

• Entertaining expenses of $10,000 which are disallowable for tax purposes

• Directors ' salaries of 530.000

Tax depreciation allowances of $60,000 are available and the rate of corporate income tax is 20%.

What is the corporate tax liability of XYZ for the reporting period?