We have coached hundreds of senior management accountants, corporate treasury analysts, and strategic finance directors through this final, high-stakes financial tier of the professional qualification. Let's look closely at the modern corporate governance training landscape. The candidates who stumble on this advanced-level evaluation are almost always those who relied on low-tier test pools—those flat, context-stripped answer repositories floating around unverified accounting forums. Those static, unverified materials simply cannot prepare you for the complex real-world investment appraisals or the multi-layered risk management trade-offs tested on the real exam. At Exact2Pass, our approach targets the underlying structural logic, capital frameworks, and risk-mitigation lifecycles of the active CIMA body of knowledge instead. Our F3 exam questions prep delivers comprehensive methodological breakdowns for every capital structure calculation and corporate restructuring scenario. You will master actual core treasury allocations instead of leaning on short-sighted memorization shortcuts. We map out Modigliani-Miller dividend irrelevance proofs, expected value decision trees, business valuation modeling methodologies, and currency swap mechanics step by step. Our learning material is built from the ground up by active Chief Financial Officers and chartered management architects who orchestrate multi-million dollar corporate strategies daily. Because of that, we completely avoid mindless, repetitive question-and-answer lists. Instead, our workspace functions as an active training simulation that forces you to evaluate corporate performance, optimal capital blend limits, and risk thresholds like a principal financial controller. You will learn the exact reason why a specific capital allocation choice or derivative hedging policy succeeds or violates corporate compliance rules. That is how you build real confidence before logging into your official Pearson VUE dashboard to clear this objective test. Our adaptive training software develops deep, practical fiscal skills that transfer perfectly to live boardrooms, helping you pass on your very first try.

A venture capitalist is most likely to take which THREE of the following exit routes?

A manufacturing company is based in Country L whose currency is the L$.

One of the company ' s products is exported to Country M, a rapidly growing economy, whose currency is the M$.

In the most recent financial year:

• 100,000 units of the product were sold to customers in country M

• The unit selling price was M$12

The spot rate today is L$1 = M$5

The company has an objective of growth in total sales value in L$ of 10% a year.

If the L$ strengthens by 5% next year against the M$, what volume of sales of this product is needed next year to achieve the objective?

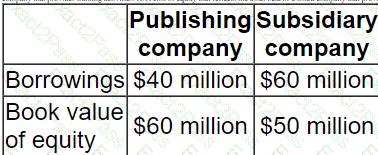

A listed publishing company owns a subsidiary company whose business activity is training.

It wishes to dispose of the subsidiary company.

The following information is available:

The board of the publishing company believe that the value of the subsidiary company, and hence the value of the equity invested in it, can be determined by calculating the present value of the subsidiary ' s free cashflows.

Which of the following is the most appropriate discount rate to use when determining the enterprise value of the company?

The Board of Directors of a listed company wish to estimate a reasonable valuation of the entire share capital of the company in the event of a takeover bid.

The company ' s current profit before taxation is $4.0 million.

The rate of corporate tax is 25%.

The average P/E multiple of listed companies in the same industry is 8 times current earnings.

The P/E multiple of recent takeovers in the same industry have ranged from 9 times to 10 times current earnings.

The average P/E multiple of the top 100 companies on the stock market is 15 times current earnings.

Advise the Board of Directors which of the following is a reasonable estimate of a range of values of the entire share capital in the event of a bid being made for the whole company?

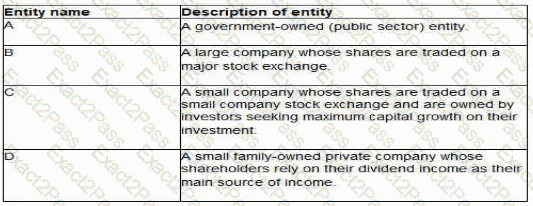

The directors of the following four entities have been discussing dividend policy:

Which of these four entities is most likely to have a residual dividend policy?

An unlisted company operates in a niche market, exploring the west coast of Africa for new oiI reservoirs.

The oil exploration program has been successful in recent years and t now has a substantial amount of oil reserves with a high level of certainty of being recoverable Under financial reporting regulations, oil still in the ground is not recognised as an asset unit is extracted.

The expense of the exploration program has used up all the company’s available cash resources.

The company has denied to list or a stock market and raise finds through an initial public offering to finance its drilling program.

Which of the following valuation methods in the appropriate to use in calculating an initial listing price for this company?

A is a listed company. Its shares trade on a stock market exhibiting semi-strong form efficiency.

Which of the following is most likely to increase the wealth of A ' s shareholders?