We have coached hundreds of senior management accountants, corporate treasury analysts, and strategic finance directors through this final, high-stakes financial tier of the professional qualification. Let's look closely at the modern corporate governance training landscape. The candidates who stumble on this advanced-level evaluation are almost always those who relied on low-tier test pools—those flat, context-stripped answer repositories floating around unverified accounting forums. Those static, unverified materials simply cannot prepare you for the complex real-world investment appraisals or the multi-layered risk management trade-offs tested on the real exam. At Exact2Pass, our approach targets the underlying structural logic, capital frameworks, and risk-mitigation lifecycles of the active CIMA body of knowledge instead. Our F3 exam questions prep delivers comprehensive methodological breakdowns for every capital structure calculation and corporate restructuring scenario. You will master actual core treasury allocations instead of leaning on short-sighted memorization shortcuts. We map out Modigliani-Miller dividend irrelevance proofs, expected value decision trees, business valuation modeling methodologies, and currency swap mechanics step by step. Our learning material is built from the ground up by active Chief Financial Officers and chartered management architects who orchestrate multi-million dollar corporate strategies daily. Because of that, we completely avoid mindless, repetitive question-and-answer lists. Instead, our workspace functions as an active training simulation that forces you to evaluate corporate performance, optimal capital blend limits, and risk thresholds like a principal financial controller. You will learn the exact reason why a specific capital allocation choice or derivative hedging policy succeeds or violates corporate compliance rules. That is how you build real confidence before logging into your official Pearson VUE dashboard to clear this objective test. Our adaptive training software develops deep, practical fiscal skills that transfer perfectly to live boardrooms, helping you pass on your very first try.

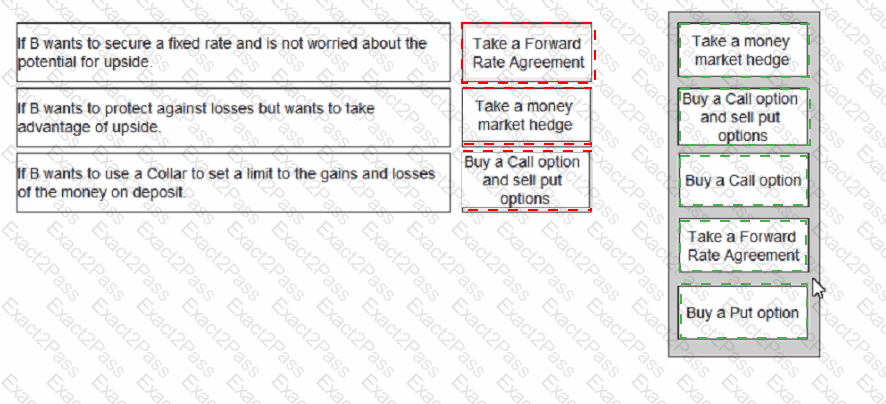

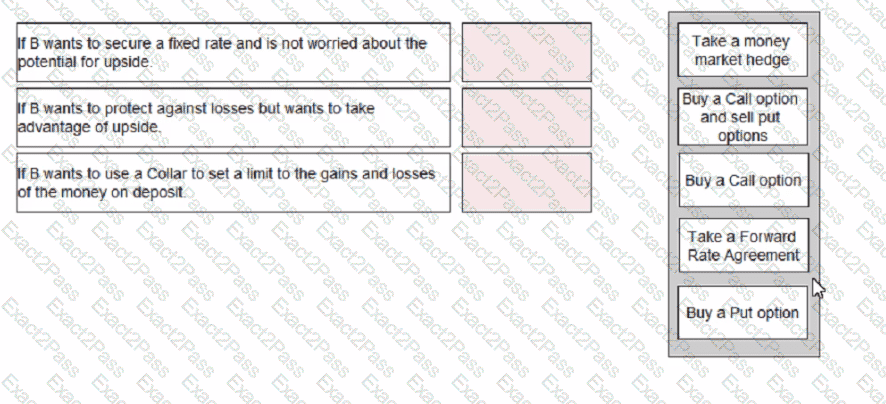

B, a European based modern art dealer, frequently imports and sells single high value items created in the United States. The price is fixed at the date of sale but the items are commissioned and made to order with a lead time of three to nine months depending on the individual specification

B holds payment for his customers from the point of purchase and passes funds when the items are shipped However, despite putting the money on short term deposit, there have been times when B ' s profits have been almost entirely eroded by adverse movements m interest rates Advise B by matching the appropriate instrument to B ' s requirements.

A company ' s Board of Directors is assessing the likely impact of financing future new projects using either equity or debt.

The directors are uncertain of the effects on key variables.

Which THREE of the following statements are true?

A company with a market capitalisation of S50million is considering raising $1 million debt to fund a new 10-year capital investment protect

The value of this issue is considered to be small in comparison to the company ' s market capitalisation

The company is considering whether to raise the debt finance by either a " bond private placing ' or a ' public bond issue.

Which THREE of the following statements are correct?

Company A is identical in all operating and risk characteristics to Company B, but their capital structures differ.

Company B is all-equity financed. Its cost of equity is 17%.

Company A has a gearing ratio (debt:equity) of 1:2. Its pre-tax cost of debt is 7%.

Company A and Company B both pay corporate income tax at 30%.

What is the cost of equity for Company A?

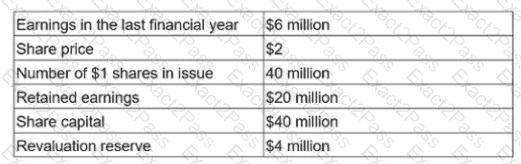

An unlisted company has the following data:

A listed company in the same industry has a P/E of 11.

The value of the unlisted company based on the P/E of this listed company is:

Give your answer to the nearest whole number.

Under traditional theory, an increase in a company ' s WACC would cause the value of the company to:

Which THREE of the following statements are true of a money market hedge?

Company C is a listed company. It is currently considering the acquisition of Company D. The original founder of Company C currently owns 52% of the shares.

Alternative forms of consideration for Company D being considered are as follows:

• Cash payment, financed by new borrowing

• issue of new shares in Company C

Which of the following is an advantage of a cash offer over a share-for exchange from the viewpoint of the original founder of Company C?

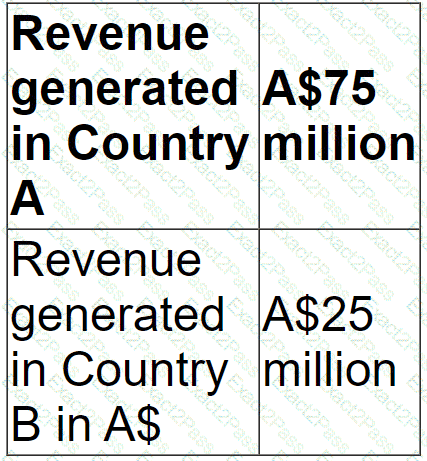

Company X is based in Country A, whose currency is the A$.

It trades with customers in Country B, whose currency is the B$.

Company X aims to maintain its revenue from exports to Country B at 25% of total revenue.

Company A has the following forecast revenue:

The forecast revenue from Country B has assumed an exchange rate of A$1/B$2, that is A$1 = B$2.

If the B$ depreciates against the A$ by 10%, the ratio of revenue generated from Country B as a percentage of total revenue will:

BBA is a wholly owned subsidiary of AAB BBA operates in country B where the currency is the B$.

The following is an extract from BBA ' s financial statements at 31 December 20X1:

The following Information is relevant:

" The bonds were trading at $110 per $100 on 31 December 20X1. " Operating profit of BBA for the year ended 31 December 20X1 was S15 million

• The P/E ratio is 8

* Corporate income tax rate is 20%.

The tax authorities m country B Implemented thin capitalisation rules based on the level of gearing of the subsidiary, calculated as book value o( debt lo book value of equity The cut-off point for gearing used by the tax authorities for a company to be thinly capitalised is 75%.

Which of the following statements is correct as at 31 December 20X1?