We have coached hundreds of senior management accountants, corporate treasury analysts, and strategic finance directors through this final, high-stakes financial tier of the professional qualification. Let's look closely at the modern corporate governance training landscape. The candidates who stumble on this advanced-level evaluation are almost always those who relied on low-tier test pools—those flat, context-stripped answer repositories floating around unverified accounting forums. Those static, unverified materials simply cannot prepare you for the complex real-world investment appraisals or the multi-layered risk management trade-offs tested on the real exam. At Exact2Pass, our approach targets the underlying structural logic, capital frameworks, and risk-mitigation lifecycles of the active CIMA body of knowledge instead. Our F3 exam questions prep delivers comprehensive methodological breakdowns for every capital structure calculation and corporate restructuring scenario. You will master actual core treasury allocations instead of leaning on short-sighted memorization shortcuts. We map out Modigliani-Miller dividend irrelevance proofs, expected value decision trees, business valuation modeling methodologies, and currency swap mechanics step by step. Our learning material is built from the ground up by active Chief Financial Officers and chartered management architects who orchestrate multi-million dollar corporate strategies daily. Because of that, we completely avoid mindless, repetitive question-and-answer lists. Instead, our workspace functions as an active training simulation that forces you to evaluate corporate performance, optimal capital blend limits, and risk thresholds like a principal financial controller. You will learn the exact reason why a specific capital allocation choice or derivative hedging policy succeeds or violates corporate compliance rules. That is how you build real confidence before logging into your official Pearson VUE dashboard to clear this objective test. Our adaptive training software develops deep, practical fiscal skills that transfer perfectly to live boardrooms, helping you pass on your very first try.

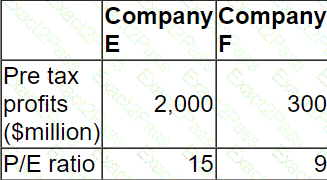

Company E is a listed company. Its directors are valuing a smaller listed company, Company F, as a possible acquisition.

The two companies operate in the same markets and have the same business risk.

Relevant data on the two companies is as follows:

Both companies are wholly equity financed and both pay corporate tax at 30%.

The directors of Company E believe they can " bootstrap " Company F ' s earnings to improve performance.

Calculate the maximum price that Company E should offer to Company F ' s shareholders to acquire the company.

Give your answer to the nearest $million.

A company currently has a 5.25% fixed rate loan but it wishes to change the interest style of the loan to variable by using an interest rate swap directly with the bank.

The bank has quoted the following swap rate:

* 4.50% - 455% in exchange for Libor

Libor is currently 4%.

If the company enters into the swap and Libor remains at 4%. what will the company ' s interest cost be?

Company X is an established, unquoted company which provides IT advisory services.

The company ' s results and cashflows are growing steadily and it has few direct competitors due to the very specialised nature of it ' s business. Dividends are predictable and paid annually.

Company P is looking to buy 30% of company X ' s equity shares.

Which TWO of the following methods are likely to be considered most suitable valuation methods for valuing company P ' s investment in Company X?

A company is funded by:

• $40 million of debt (market value)

• $60 million of equity (market value)

The company plans to:

• Issue a bond and use the funds raised to buy back shares at their current market value.

• Structure the deal so that the market value of debt becomes equal to the market value of equity.

According to Modigliani and Miller ' s theory with tax and assuming a corporate income tax rate of 20%, this plan would:

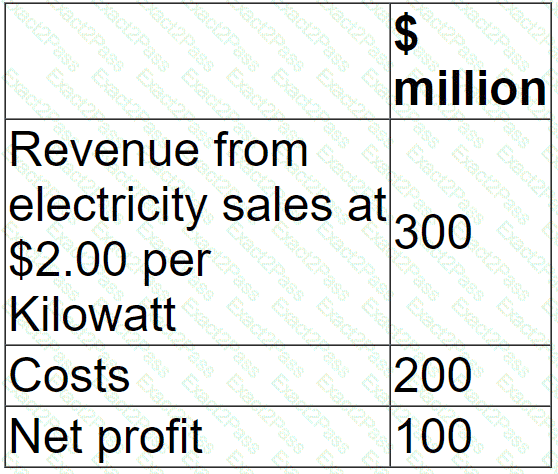

A company generates and distributes electricity and gas to households and businesses.

Forecast results for the next financial year are as follows:

The Industry Regulator has announced a new price cap of $1.50 per Kilowatt.

The company expects this to cause consumption to rise by 10% but costs would remained unaltered.

The price cap is expected to cause the company ' s net profit to fall to:

The directors of a multinational group have decided to sell off a loss-making subsidiary and are considering the following methods of divestment:

1. Trade sale to an external buyer

2. A management buyout (MBO)

The MBO team and the external buyer have both offered the same price to the parent company for the subsidiary.

Which of the following is an advantage to the parent company of opting for a MBO compared to a trade sale as the preferred method of divestment?

A company has undertaken a transaction with its shareholders which has had the following impact on its financial statements:

• Retained earnings has decreased

• Share capital has increased

• Earnings per share has decreased

• The book value of equity is unchanged

The company has undertaken a:

Which of the following statements about the tax impact on debt finance is correct?

A new company was set up two years ago using the personal financial resources of the founders.

These funds were used to acquire suitable premises.

The company has entered into a long-term lease on the premises which are not yet fully fitted out.

The founders are considering requesting loan finance from the company ' s bank to fund the purchase of custom-made advanced technology equipment.

No other companies are using this type of equipment.

The company expects to continue to be profitable for the forseeable future.

It re-invests some of its surplus cash in on-going essential research and development.

Which THREE of the following features are likely to be considered negatives by the bank when assessing the company ' s credit-worthiness?

An unlisted company wishes to obtain an estimated value for its shares in anticipation of a private sale of a large parcel of shares.

Relevant data for the unlisted company:

• It has a residual dividend policy.

• It has earnings that are highly sensitive to underlying economic conditions.

• It is a small business in a large industry where there are listed companies but there are none with a similar capital structure.

The company intends to base valuations on the cost of equity of a proxy company after adjusting for any differences in capital structure where appropriate.

Which of the following methods is likely to give the most accurate equity value for this unlisted company?