We have coached hundreds of senior management accountants, corporate treasury analysts, and strategic finance directors through this final, high-stakes financial tier of the professional qualification. Let's look closely at the modern corporate governance training landscape. The candidates who stumble on this advanced-level evaluation are almost always those who relied on low-tier test pools—those flat, context-stripped answer repositories floating around unverified accounting forums. Those static, unverified materials simply cannot prepare you for the complex real-world investment appraisals or the multi-layered risk management trade-offs tested on the real exam. At Exact2Pass, our approach targets the underlying structural logic, capital frameworks, and risk-mitigation lifecycles of the active CIMA body of knowledge instead. Our F3 exam questions prep delivers comprehensive methodological breakdowns for every capital structure calculation and corporate restructuring scenario. You will master actual core treasury allocations instead of leaning on short-sighted memorization shortcuts. We map out Modigliani-Miller dividend irrelevance proofs, expected value decision trees, business valuation modeling methodologies, and currency swap mechanics step by step. Our learning material is built from the ground up by active Chief Financial Officers and chartered management architects who orchestrate multi-million dollar corporate strategies daily. Because of that, we completely avoid mindless, repetitive question-and-answer lists. Instead, our workspace functions as an active training simulation that forces you to evaluate corporate performance, optimal capital blend limits, and risk thresholds like a principal financial controller. You will learn the exact reason why a specific capital allocation choice or derivative hedging policy succeeds or violates corporate compliance rules. That is how you build real confidence before logging into your official Pearson VUE dashboard to clear this objective test. Our adaptive training software develops deep, practical fiscal skills that transfer perfectly to live boardrooms, helping you pass on your very first try.

On 1 January:

• Company ABB has a value of $55 million

• Company BBA has a value of $25 million

• Both companies are wholly equity financed

Company ABB plans to take over Company BBA by means of a share exchange Following the acquisition the post-tax cashflow of Company ABB for the foreseeable future is estimated to be $10 million each year The post-acquisition cost of equity is expected to be 10%

What is the best estimate of the value of the synergy that would arise from the acquisition?

Which of the following best explains why the interest rate parity model is highly effective in practice?

STU has relatively few tangible assets and is dependent for profits and growth on the high-value individuals it employs. Which of the following statements best explains why the net asset valuator method’s considered unstable for TU?

The Board of Directors of a listed company wish to estimate a reasonable valuation of the entire share capital of the company in the event of a takeover bid.

The company ' s current profit before taxation is $10 0 million.

The rate of corporate tax is 20%.

The average P/E multiple of listed companies in the same industry is 10 times current earnings.

The P/E multiple of recent takeovers in the same industry have ranged from 11 times to 12 times current earnings.

The average P/E multiple of the top 100 companies on the stock market is 16 times current earnings.

Advise the Board of Directors which of the following is a reasonable estimate of a range of values of the entire share capital in the event of a bid being made for the whole company?

Company A is based in Country A where the functional currency is the A$. Currently all sales are to domestic customers in Country A. However, the company is planning to expand internationally by acquiring Company B, a distribution company in Country B, to enable it to sell goods worldwide The functional currency of Country B is the BS

Company A will invoice its international customers in their local currency.

Wage increases in Country B are forecast to be modest, due to high unemployment levels, but overall inflation in Country B is forecast to be significantly higher than in Country A

Which TWO of the following statements about the economic risk of the acquisition of Company B are true?

A large multi-divisional company in the food processing and distribution business is conducting a strategic review. The divisions all compete in the same market.

The sale of one of its underperforming food processing divisions to the divisional management team is currently being considered. The purchase by the divisional management team will require venture capital finance.

Which THREE of the following are likely to influence the multi-divisional company ' s decision on whether or not to sell the under-performing division to the management team?

ZZZ is a listed company based in Brinland. a European country. It is the largest owner and operator of residential care homes for elderly people in Brinland

Most of the residential care homes in Brinland are run by small private operators, and the standards of cafe are extremely variable However. 22Z has developed a good reputation because its client service is considered to be extremely good even though its prices are higher than those of most of its competitors.

ZZZ has expanded rapidly in the last few years, partly by acquisition and partly by organic growth consequently, the company ' s share price now stands at a record high, and the dividend declared at the end of the most recent accounting period was 10% higher than the previous year ' s dividend.

The Brinland government has recently set up a regulatory body to monitor the residential care homes industry. The regulatory body is considering introducing a variety of regulations to improve the customer experience in the industry. Following a period of consultation and investigation, the regulatory body is expected to announce a range of new regulations in the near future.

The directors of ZZZ are concerned that the new regulations may adversely affect their company

Which THREE of the following new regulations are likely to have the greatest negative impact on ZZTs performance?

Company A is planning to acquire Company B at a price of $ 65 million by means of a cash bid.

Company A is confident that the merged entity can achieve the same price earnings ratio as that of Company A.

What does Company A expect the value of the merged entity to be post acquisition?

Company BBB has prepared a valuation of a competitor company, Company BBD. Company BBB is intending to acquire a controlling interest in the equity of Company BBD and therefore wants to value only the equity of Company BBD.

The directors of Company BBB have prepared the following valuation of Company BBD:

Value of Equity = 4.63 + 5.14 + 5.56 = S15.33 million

Additional information on Company BBD:

Which THREE of the following are weaknesses of the above valuation?

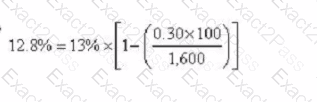

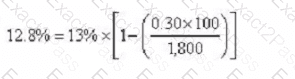

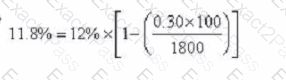

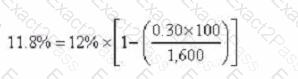

Company M is a geared company whose equity has a market value of $1,500 million and debt has a market value of S300 million. The company plans to issue $200 million of new shares and use the funds raised to pay off some of the debt

Company M currently has a cost of equity of 13% and a WACC of 10% It pays corporate tax at the rate of 30% Company B, an ungeared company operating in the same business sector as Company M, has a cost of equity of 12%

Assume Modigliani and Miller ' s theory of capital structure with tax applies

Which calculation below shows the correct approach to calculating the new WACC following the planned changes in capital structure?

A

B

C

D