We have coached hundreds of senior management accountants, corporate treasury analysts, and strategic finance directors through this final, high-stakes financial tier of the professional qualification. Let's look closely at the modern corporate governance training landscape. The candidates who stumble on this advanced-level evaluation are almost always those who relied on low-tier test pools—those flat, context-stripped answer repositories floating around unverified accounting forums. Those static, unverified materials simply cannot prepare you for the complex real-world investment appraisals or the multi-layered risk management trade-offs tested on the real exam. At Exact2Pass, our approach targets the underlying structural logic, capital frameworks, and risk-mitigation lifecycles of the active CIMA body of knowledge instead. Our F3 exam questions prep delivers comprehensive methodological breakdowns for every capital structure calculation and corporate restructuring scenario. You will master actual core treasury allocations instead of leaning on short-sighted memorization shortcuts. We map out Modigliani-Miller dividend irrelevance proofs, expected value decision trees, business valuation modeling methodologies, and currency swap mechanics step by step. Our learning material is built from the ground up by active Chief Financial Officers and chartered management architects who orchestrate multi-million dollar corporate strategies daily. Because of that, we completely avoid mindless, repetitive question-and-answer lists. Instead, our workspace functions as an active training simulation that forces you to evaluate corporate performance, optimal capital blend limits, and risk thresholds like a principal financial controller. You will learn the exact reason why a specific capital allocation choice or derivative hedging policy succeeds or violates corporate compliance rules. That is how you build real confidence before logging into your official Pearson VUE dashboard to clear this objective test. Our adaptive training software develops deep, practical fiscal skills that transfer perfectly to live boardrooms, helping you pass on your very first try.

Which of the following statements are true with regard to interest rate swaps?

Select ALL that apply.

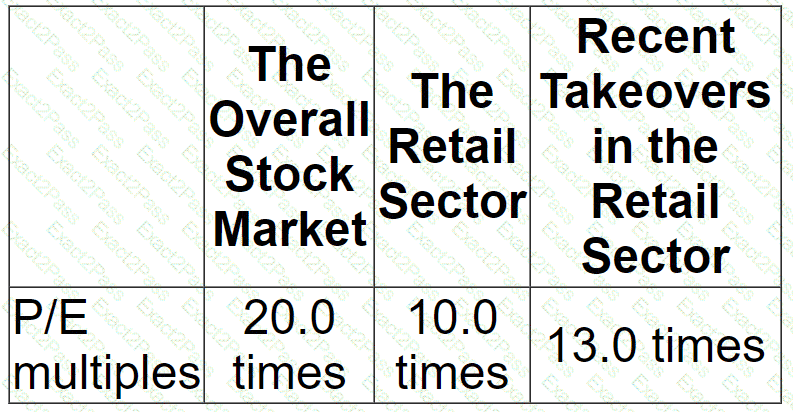

Company HJK is planning to bid for listed company BNM

Financial data for BNM for the financial year ended 31 December 20X1:

HJK is not forecasting any growth in these figures for the foreseeable future

Profit and cost data above should be assumed to be equivalent to cash flow data when answenng this question

Which THREE of the following approaches would be most appropriate for HJK to use to value the equity of BNM?

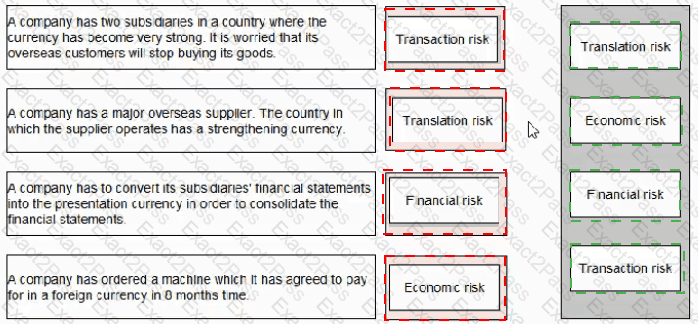

Select the category of risk for each of the descriptions below:

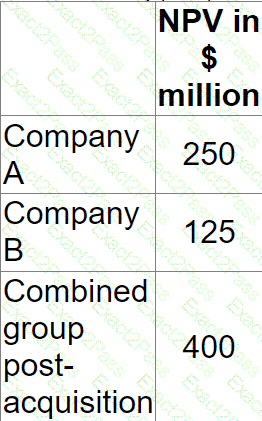

Company A is planning to acquire Company B by means of a cash offer. The directors of Company B are prepared to recommend acceptance if a bid price can be agreed. Estimates of the net present value (NPV) of future cash flows for the two companies and the combined group post acquisition have been prepared by Company A’s accountant. There are as follows:

What is the maximum price that Company A should offer for the shares in Company B?

Give your answer to the nearest $ million

A company needs to raise $20 million to finance a project.

It has decided on a rights issue at a discount of 20% to its current market share price.

There are currently 20 million shares in issue with a nominal value of $1 and a market price of $5 per share.

Calculate the terms of the rights issue.

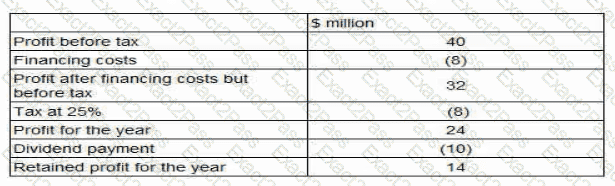

An all equity financed company reported earnings for the year ending 31 December 20X1 of $5 million.

One of its financial objectives is to increase earnings by 5% each year.

In the year ending 31 December 20X2 it financed a project by issuing a bond with a $1 million nominal value and a coupon rate of 7%.

The company pays corporate income tax at 30%.

If the company is to achieve its earnings target for the year ending 31 December 20X2, what is the minimum operating profit (profit before interest and tax) that it must achieve?

SUP is a large supermarket chain. It produces many ' own brand ' goods in Country S where the parent company is located. These goods are sold in SUP ' s supermarkets in Country S as well as being sold at a ' transfer price ' to SUP companies located in foreign countries for sale in the SUP supermarkets located in that country.

Which of the following factors is the most important for SUP from a lax planning and compliance viewpoint when setting prices for the ' own brand ' goods sold to other group companies ' ?

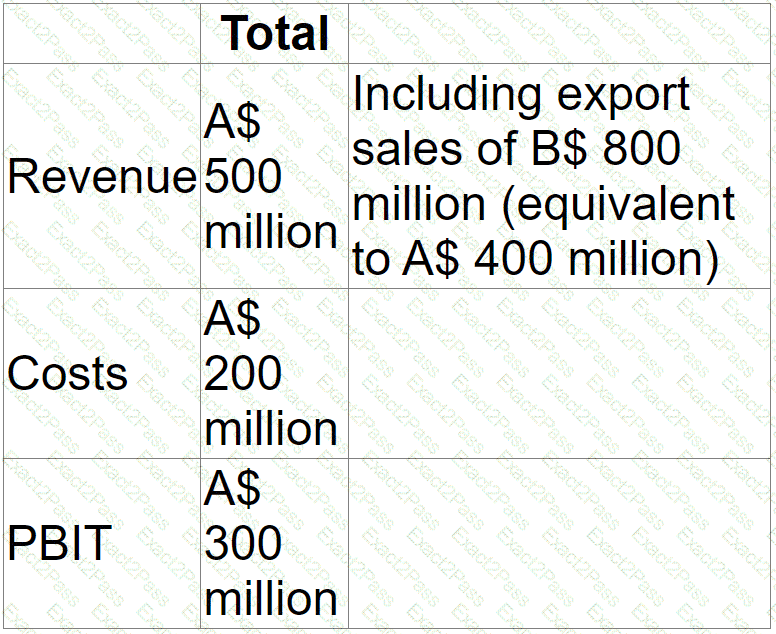

A company aims to increase profit before interest and tax (PBIT) each year.

The company reports in A$ but has significant export sales priced in B$.

All other transactions are priced in A$.

In 20X1, the company reported:

In 20X2, the only changes expected are:

• An increase in export prices of 10%, but no change to units sold.

• A rise in the value of the B$ to A$/B$ 2.500 (that is, A$ 1 = B$ 2.5)

Is it likely that the company would still meet its objective to grow PBIT between 20X1 and 20X2?

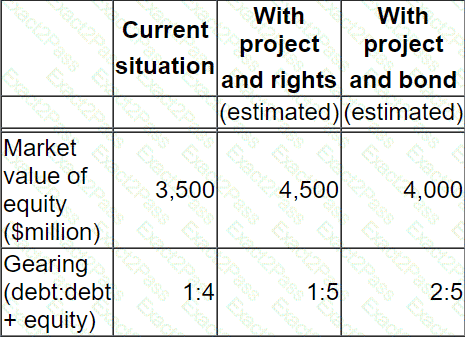

A listed company plans to raise $350 million to finance a major expansion programme.

The cash flow projections for the programme are subject to considerable variability.

Brief details of the programme have been public knowledge for a few weeks.

The directors are considering two financing options, either a rights issue at a 20% discount to current share price or a long term bond.

The following data is relevant:

The company ' s share price has fallen by 5% over the past 3 months compared with a fall in the market of 3% over the same period.

The directors favour the bond option.

However, the Chief Accountant has provided arguments for a rights issue.

Which TWO of the following arguments in favour of a right issue are correct?

The Board of Directors of a listed company have decided that it needs to increase its equity capital to ensure it is in a more stable financial position.

The shareholder profile is a mix of institutional and individual small shareholders.

The board is considering either:

• A scrip dividend

• A zero dividend

Which THREE of the following would be considered disadvantages of a scrip dividend compared to a zero dividend?