We have coached hundreds of senior management accountants, corporate treasury analysts, and strategic finance directors through this final, high-stakes financial tier of the professional qualification. Let's look closely at the modern corporate governance training landscape. The candidates who stumble on this advanced-level evaluation are almost always those who relied on low-tier test pools—those flat, context-stripped answer repositories floating around unverified accounting forums. Those static, unverified materials simply cannot prepare you for the complex real-world investment appraisals or the multi-layered risk management trade-offs tested on the real exam. At Exact2Pass, our approach targets the underlying structural logic, capital frameworks, and risk-mitigation lifecycles of the active CIMA body of knowledge instead. Our F3 exam questions prep delivers comprehensive methodological breakdowns for every capital structure calculation and corporate restructuring scenario. You will master actual core treasury allocations instead of leaning on short-sighted memorization shortcuts. We map out Modigliani-Miller dividend irrelevance proofs, expected value decision trees, business valuation modeling methodologies, and currency swap mechanics step by step. Our learning material is built from the ground up by active Chief Financial Officers and chartered management architects who orchestrate multi-million dollar corporate strategies daily. Because of that, we completely avoid mindless, repetitive question-and-answer lists. Instead, our workspace functions as an active training simulation that forces you to evaluate corporate performance, optimal capital blend limits, and risk thresholds like a principal financial controller. You will learn the exact reason why a specific capital allocation choice or derivative hedging policy succeeds or violates corporate compliance rules. That is how you build real confidence before logging into your official Pearson VUE dashboard to clear this objective test. Our adaptive training software develops deep, practical fiscal skills that transfer perfectly to live boardrooms, helping you pass on your very first try.

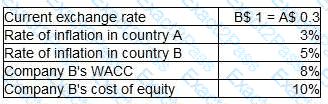

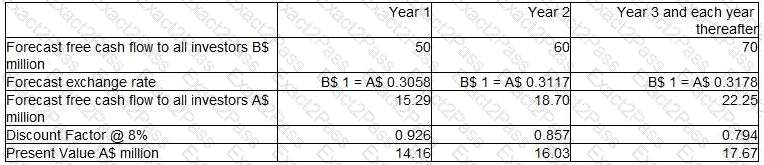

Company A operates in country A and uses currency AS. It is looking to acquire Company B which operates in country B and uses currency B$. The following information is relevant:

The assistant accountant at Company A has prepared the following valuation of company B ' s equity, however there are some errors in his calculations.

Value of Company B ' s equity = 14.16 + 16.03 + 17.67 = AS47.86 million

Company B has BS5 million of debt finance.

Which of the following THREE statements are true?

XYZ has a variable rate loan of $200 million on which it is paying interest of Liber ‘3%.

XYZ entered into a swap with AG bank to convert this to a fixed rate 8% loan. AB bank charges an annual commission of 0.4% for making this arrangement

Calculate the net payment from KYZ to AB bank at the end of the first year if Libor was 2% throughout the year.

Give your answer in $ million, to one decimal place.

A company based in Country A with the A$ as its functional currency requires A$500 million 20-year debt finance to finance a long-term investment The company has a high credit rating, but has not previously issued corporate bonds which are listed on the stock exchange Which THREE of the following are advantages of issuing 20 year bonds compared with simply borrowing for a 20 year period?

A company has two divisions.

A is the manufacturing division and supplies only to B, the retail division.

The Board of Directors has been approached by another company to acquire Division B as part of their retail expansion programme.

Division A will continue to supply to Division B as a retail customer as well as source and supply to other retail customers.

Which is the main risk faced by the company based on the above proposal?

The two founding directors of an unlisted geared company want to establish its value as they are intending to approach a venture capitalist for additional funding.

The funding will be used to invest in a major new project which has very high growth potential. The directors intend to sell 10% of the company to the venture capitalist They have prepared the following current valuation of the company using the divided valuation model:

The following information is relevant.

• $60,000 is the most recent dividend paid.

• 4% is the average dividend growth over the last few years.

• 10% is an estimate of the company ' s cost of equity using the CAPM model with the industry average asset beta

Which THREE of the following are weaknesses of the valuation method used in these circumstances?

The long-term prospects for inflation in the UK and the USA are 1% and 4% per annum respectively.

The GBP/USD spot rate is currently GBP/USD1.40

Using purchasing power parity theory, what GBP/USD spot rate would you expect to see in six months’ time?

A company has just received a hostile bid. Which of the following response strategies could be considered?

KKL is a listed sports clothing company with three separate business units. KKL is seeking to sell TT’, one of these business units

TTP cwns a new. brand of trail running shoes that have Droved hugely popular with lone distance runners. The management team of TTP are frustrated by the constraints imposes b/ KKL in managing tie brand and developing. the bus ness and they believe that TTF has huge growth potential.

The management team of TTP have approached KKL with a proposal to purchase 1~P through a management layout (MDO). KKL has accepted this proposal as TTP has not proved to be a good fit ' with the rest of the business and has agreed on the selling price.

Which THREE of the following factors a-e mast Likely to affect the success of the MBO?

A company is reporting under IFRS 7 Financial Instruments: Disclosures for the first time and the directors are concerned about whether this will lead to the disclosure of information that could affect the company ' s share price.

The company is based in a country that uses the A$ but 40% of revenue relates to export sales to the USA and priced in US$.

When the company reports under IFRS 7 for the first time, the share price is most likely to:

Company A, a listed company, plans to acquire Company T, which is also listed.

Additional information is:

• Company A has 150 million shares in issue, with market price currently at $7.00 per share.

• Company T has 120 million shares in issue,. with market price currently at $6.00 each share.

• Synergies valued at $50 million are expected to arise from the acquisition.

• The terms of the offer will be 2 shares in A for 3 shares in T.

Assuming the offer is accepted and the synergies are realised, what should the post-acquisition price of each of Company A ' s shares be?

Give your answer to two decimal places.